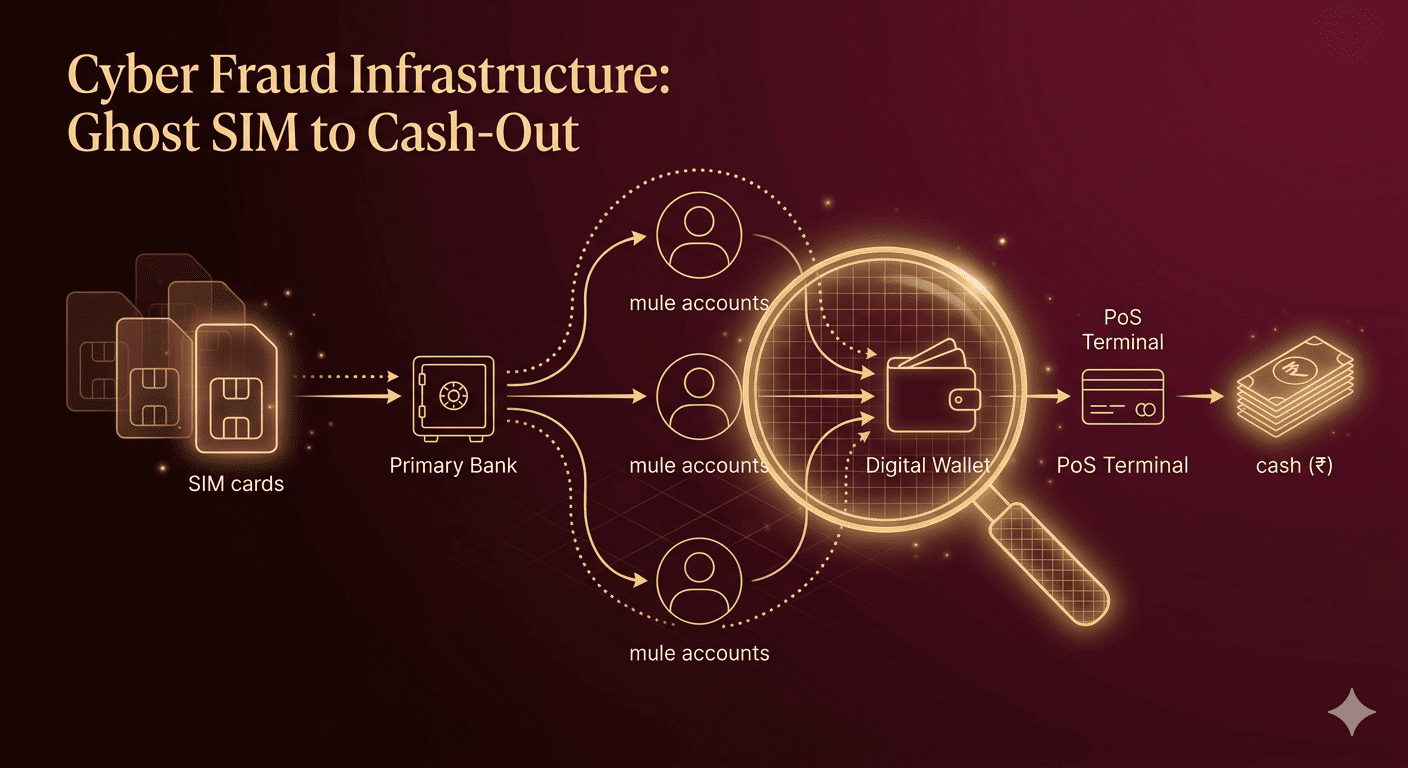

Ghost SIMs and PoS Agents: Exposing the Hidden Backend of India’s Cyber Fraud Network

Ghost SIMs and rogue PoS agents form the invisible backbone of India’s cyber fraud ecosystem. This visual breakdown explains how stolen KYC data is used to issue ghost SIMs, activate mule bank accounts, route funds through digital wallets, and ultimately cash out via PoS terminals. It offers a clear, end-to-end view of how organised fraud networks operate behind the scenes.