Waking up to a frozen bank account is one of the most stressful financial experiences an Indian citizen can face. Your salary cannot be withdrawn. Your bills cannot be paid. Your business operations may have ground to a halt. And the bank is giving you very little information about what happened or why.

This guide is written specifically for you. Whether your account was frozen due to a cybercrime complaint, a UPI dispute, a cryptocurrency transaction, or any other fraud-related investigation, this article will walk you through everything — what happened, why it happened, what your rights are, and exactly what to do next.

Table of Contents

Why Is My Account Frozen and What Should I Do?

Bank accounts in India are frozen when banks, police, cybercrime authorities, or courts suspect that an account has received or processed funds linked to fraud, money laundering, or other financial crimes. The freeze prevents withdrawals to preserve funds for investigation.

The good news: Most legitimate account holders — especially those who were unknowingly caught in fraud transactions — can get their accounts unfrozen by cooperating with investigating authorities, providing documentary evidence, and following the correct process.

Act immediately. Every day of delay prolongs the freeze.

Quick Summary Table

| Question | Answer |

| Can a frozen account be unfrozen? | Yes, in most cases, with cooperation and documentation |

| Who freezes accounts? | Banks, police, cybercrime cells, courts, RBI, ED |

| How long does it take? | 1 week to 12+ months depending on freeze type |

| Common reasons | Fraud complaints, suspicious UPI transactions, crypto P2P, KYC issues, court orders |

| First step | Visit branch, get written reason for freeze, preserve all transaction records |

| Legal remedies | Banking Ombudsman, Consumer Forum, Writ Petition, Criminal Court |

| Chances of success | High if innocent and cooperative; moderate if funds traced to fraud |

What Does a Frozen Bank Account Mean?

A “frozen account” is a broad term. The actual restrictions on your account depend on the type of freeze applied. Understanding the distinction is critical because it determines what you can and cannot do with your money.

| Freeze Type | What It Means | Can You Receive Money? | Can You Withdraw? |

| Full Freeze | No incoming or outgoing transactions | No | No |

| Debit Freeze | Can receive money; cannot withdraw or transfer | Yes | No |

| Credit Freeze | Cannot receive money; can withdraw existing balance | No | Yes |

| Partial Freeze | Only certain transactions blocked | Depends | Depends |

| Lien Marking | A specific amount is blocked; rest is accessible | Yes | Only non-liened amount |

| Hold Marking | Amount held pending investigation or dispute | Yes | Only un-held amount |

Debit freeze is the most common type applied in fraud and cybercrime cases. Your salary and other credits may still land in your account — but you cannot touch the money until the freeze is lifted.

A lien is specifically a claim on a defined portion of your funds. If the lien amount is ₹50,000 and you have ₹1,20,000 in your account, you can access ₹70,000.

Why Banks Freeze Accounts in India

Cybercrime Complaints

This is the single largest reason for account freezes in India today. When a fraud victim files a complaint at cybercrime.gov.in or calls helpline 1930, the cyber crime system triggers an automated or manual alert to the bank associated with the account that received the fraudulent funds. The bank freezes the account to prevent further movement of fraud proceeds.

The account frozen is not always the fraudster’s account. Often it is the account of a person who received the money unknowingly — through a part-time job payment, a P2P crypto trade, or a simple bank transfer from someone they did not know was a fraud victim.

Who initiates it: Cybercrime cell or portal system How to respond: Contact the cybercrime cell that initiated the complaint and provide evidence that your transaction was legitimate

Fraud Investigations

When a bank’s internal fraud monitoring system identifies unusual patterns — sudden large deposits, rapid transfer-outs, geographic inconsistencies — it may freeze the account pending internal review. Banks have RBI-mandated Anti-Money Laundering systems that flag these patterns automatically.

Who initiates it: Bank’s internal fraud or compliance team How to respond: Visit branch with income and transaction proof

Suspicious UPI Transactions

UPI has made digital payments instant and seamless — but the same speed makes it attractive for fraud. When fraud victims report UPI payment fraud, NPCI and the bank initiate a dispute process that can result in the recipient’s account being frozen pending reversal.

Who initiates it: Victim’s bank, NPCI, or RBI direction How to respond: Provide evidence that the UPI payment you received was legitimate

KYC Issues

Accounts where KYC (Know Your Customer) documentation is incomplete, outdated, or flagged as potentially fraudulent are frozen. This is a compliance-driven freeze rather than a crime-investigation freeze, and it is generally the easiest to resolve.

Who initiates it: Bank compliance department How to respond: Visit branch and update KYC documents

Court Orders

Courts — including civil courts, criminal courts, and High Courts — can order account freezes as part of legal proceedings. These freezes are legally the most complex to challenge and require proper legal representation.

Who initiates it: Court order served on bank How to respond: Engage a lawyer to appear in the relevant court

Police Requests

State and local police investigating financial crimes can direct banks to freeze accounts. These requests can be informal letters or formal Section 102 CrPC (now BNSS) seizure orders. Informal police letters do not have the same legal authority as court orders, but banks often comply regardless.

Who initiates it: Police investigation officer How to respond: Engage with the investigating officer’s station; engage a lawyer

Regulatory Directions

RBI, SEBI, or ED can direct freezes as part of systemic or regulatory actions. These are most common in large organized fraud cases.

Who initiates it: RBI / SEBI / ED How to respond: Engage legal counsel specializing in financial regulations

Crypto-Related Transactions

Accounts involved in cryptocurrency P2P trading — particularly receiving INR from buyers on platforms like Binance P2P or LocalBitcoins — face increasing freeze risk. If the person who paid you INR had obtained those funds through fraud, your account may be flagged.

Who initiates it: Cybercrime cell, bank compliance, or ED How to respond: Provide P2P trade records, exchange screenshots, and KYC documentation

Money Laundering Concerns

When an account shows patterns consistent with layering — receiving large amounts and quickly transferring them out in smaller pieces — it triggers AML (Anti-Money Laundering) alerts. This can happen even to legitimate businesses.

Who initiates it: Bank’s AML system, FIU-IND How to respond: Provide business transaction documentation and income proof

Mule Account Investigations

Mule accounts are bank accounts used — knowingly or unknowingly — to layer fraud proceeds. People who rented their accounts, shared credentials, or simply received funds from fraudsters are flagged as mule accounts.

Who initiates it: Cybercrime police, bank How to respond: Cooperate fully; demonstrate you did not knowingly participate

Most Common Reasons Accounts Get Frozen in 2026

- Receiving UPI payments from fraud victims: The most common trigger. When a fraud victim reverses a UPI complaint, your receiving account gets flagged.

- Crypto P2P INR receipts: Receiving bank transfers from crypto buyers whose source of funds is flagged.

- Frequent high-value cash deposits: Triggers AML alerts, especially without corresponding income documentation.

- Account renting: Allowing others to use your account for payments in exchange for commission — a practice that is illegal and directly creates mule account liability.

- Receiving funds from lottery or prize scams: Scam operators send advance funds to victims to establish trust; victim’s account may be flagged as a receiving account.

- Online job scams: Part-time job schemes where victims are paid to receive and forward money — account is used as a mule without the victim realizing it.

- SIM swap fraud: Fraudster takes over phone number, accesses mobile banking, and conducts unauthorized transfers from victim’s account — then the victim’s account is investigated.

- Chargeback disputes on e-commerce: Merchant accounts face freezes when multiple chargebacks are filed.

- Identity theft: Someone opened an account using your KYC documents; that account’s activities flag your legitimate account.

- Investment scheme payouts: Receiving referral commissions or payouts from Ponzi or MLM schemes can trigger AML flags.

- Rapid round-tripping: Receiving and immediately transferring the same amount to another account — classic layering pattern.

- Multiple accounts with similar transaction patterns: Banks identify clusters of accounts operating similarly and flag all of them.

- Telegram or WhatsApp payment scheme involvement: Receiving payments as part of “task-based” online earning schemes often linked to cybercrime.

- Overseas remittance irregularities: Receiving foreign transfers that do not match stated purpose triggers FEMA review.

- KYC mismatch: Photo, name, or address discrepancies in KYC documentation.

- Dormant account suddenly activated: Sudden high-value activity in a long-dormant account triggers review.

- Court attachment: Civil court orders attaching accounts as part of debt recovery or matrimonial proceedings.

- Tax authority directions: Income Tax Department can direct freezes during investigation.

- Phishing victim’s account investigated: If your credentials were stolen and fraudulent transactions occurred, your account may itself be investigated.

- Fraudulent cheque deposits: Depositing a cheque that turns out to be fraudulent can result in your account being held.

Can Banks Freeze Accounts Without Notice?

This is one of the most commonly asked questions — and the answer is nuanced.

In general, banks should notify customers. RBI guidelines require banks to inform customers of account restrictions. However, in practice, notification is often delayed or inadequate, especially in cybercrime investigation freezes where banks receive government directions to act immediately and confidentially.

| Situation | Prior Notice Likely? | Explanation |

| KYC compliance freeze | Yes | Bank typically sends SMS and email before freezing |

| Bank’s internal fraud review | Sometimes | May freeze first and inform later |

| Cybercrime cell direction | Rarely | Investigation confidentiality often prevents prior notice |

| Police request (informal letter) | Rarely | Account frozen before customer is informed |

| Court order | No | Order served on bank; customer may learn from bank or court |

| RBI/ED regulatory direction | No | Regulatory authority may restrict notice |

| Inoperative account review | Yes | Banks send advance notice to activate dormant accounts |

Even when notice is not given in advance, you are entitled to know the reason for the freeze after it is applied. Request this information in writing from your bank.

How to Find Out Why Your Account Was Frozen

Many victims discover their account is frozen at an ATM or while making a UPI payment. The bank rarely explains why at that moment. Here is how to find out.

Step 1: Call Customer Care

Call your bank’s customer care number immediately. Ask specifically: “My account is frozen. Can you tell me the reason and the reference number for the freeze order?” Note the name of the representative and the time of the call.

Step 2: Visit Your Home Branch

Go to the branch where your account is held. Do not go to any other branch. Ask to speak to the Branch Manager or Relationship Manager. Carry your passbook, Aadhaar, and PAN.

Step 3: Request Written Clarification

Submit a written application (addressed to the Branch Manager) requesting the specific reason for the freeze, the name of the authority that directed it, the freeze reference number or order number, and the documents required to resolve the freeze.

Step 4: Check for Notices or Legal Communications

Check your registered email, SMS, and postal address. Cybercrime cells sometimes send notices. Check if any court documents have been served at your address.

Step 5: Check Cybercrime Portal

Visit cybercrime.gov.in and check if any complaint references your account number. You may also call 1930 to enquire.

Step 6: Contact the Investigating Authority Directly

Once you know whether the freeze is from police, cybercrime cell, or court, contact that authority directly. For police freezes, visit the relevant police station. For cybercrime cell freezes, contact the State Cyber Cell.

Account Freeze Investigation Checklist

| Action | Done? |

| Called bank customer care | ☐ |

| Visited home branch | ☐ |

| Submitted written clarification request | ☐ |

| Obtained freeze reference number | ☐ |

| Received written reason for freeze | ☐ |

| Identified initiating authority | ☐ |

| Checked for notices at registered address | ☐ |

| Checked cybercrime portal | ☐ |

| Contacted investigating officer | ☐ |

| Consulted a lawyer | ☐ |

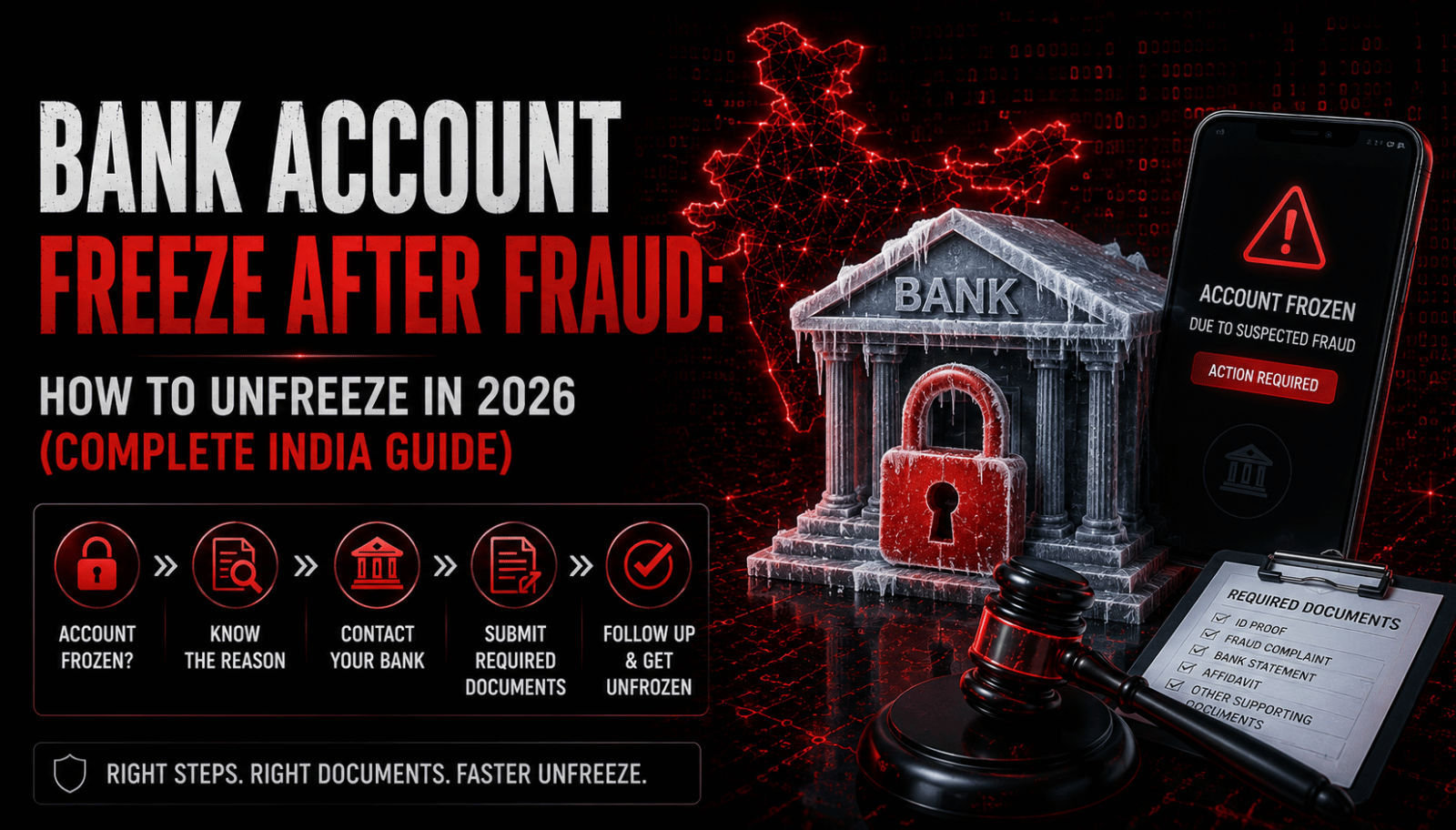

Step-by-Step Process to Unfreeze a Bank Account

This is the most important section of this guide. Follow these steps in order.

Step 1: Confirm the Exact Freeze Reason

Do not assume. Different freeze reasons require completely different resolution paths. A KYC freeze is resolved at the branch. A cybercrime freeze requires engaging with police. A court order freeze requires a lawyer in the relevant court.

Get the reason in writing before doing anything else.

Step 2: Obtain Freeze Order Details

Ask for the freeze order number, the name and designation of the officer who issued it, the police station or court reference, and the specific complaint or case number associated with the freeze.

This information is essential for every subsequent step.

Step 3: Collect Relevant Documents

Based on the freeze reason, assemble your documents. See the full document table in the next section.

Step 4: Submit a Written Explanation to the Bank

Write a formal letter to the Branch Manager explaining the nature of your transactions, why your account should not be frozen, and attaching supporting documents. Keep a copy of everything you submit.

This letter creates a formal record that you cooperated and provided information.

Step 5: Contact the Investigating Authority Directly

If the freeze was initiated by police or cybercrime cell, visit or write to the relevant authority. Introduce yourself as the account holder, explain that you are cooperating fully, and provide your documentary evidence.

Do not be defensive or aggressive. Cooperation speeds up resolution significantly.

Step 6: Respond to All Notices Within Deadlines

If you receive any notice — from the bank, police, cybercrime cell, or court — respond within the stated deadline. Missing deadlines can result in escalated action, including charge sheets or contempt proceedings.

If you do not understand a notice, consult a lawyer before responding.

Step 7: Engage Legal Representation if Required

If the freeze is related to a police investigation, court order, or ED action, engage a lawyer. Attempting to navigate these processes without legal advice is risky.

Look for advocates who specialize in cybercrime defense, banking law, or financial fraud cases.

Step 8: Follow Up Consistently and in Writing

Do not rely on verbal assurances from bank staff or police. Every follow-up should be in writing — email or written letter with acknowledgment. This creates a paper trail that is valuable if you need to escalate.

Follow up every 7–10 days.

Step 9: Escalate if No Response

If the bank does not respond to your written requests within a reasonable time (typically 30 days), escalate to:

- Banking Ombudsman (RBI)

- Consumer Forum

- State Cyber Cell Superintendent

- High Court (Writ Petition)

Step 10: Account Restoration Confirmation

Once the freeze is lifted, verify in writing that all restrictions have been removed. Test your account with a small transaction. Ensure UPI, net banking, and ATM access are all restored. Obtain a written confirmation from the bank that the freeze has been fully lifted.

Documents Required to Unfreeze an Account

| Document | Purpose | Why It May Be Needed |

| Aadhaar Card | Identity proof | Confirm account holder identity |

| PAN Card | Financial identity | Tax identity, high-value transaction verification |

| Bank Account Statement (6–12 months) | Transaction history | Demonstrate normal transaction patterns |

| Salary Slips or Form 16 | Income proof | Explain source of deposits |

| Business Invoices / GST Returns | Business income proof | Explain large credits for business accounts |

| ITR (Income Tax Return) | Financial legitimacy | Demonstrate tax compliance |

| Employment Letter | Employment verification | Support income source claims |

| Trade/Transaction Proofs | Legitimacy of specific transactions | Prove a specific flagged transaction was legitimate |

| Communication Records | Evidence of relationship | Prove you knew the sender legitimately |

| Cryptocurrency Exchange Records | Crypto transaction proof | Prove P2P trades were on regulated platforms |

| UPI Transaction Screenshots | UPI payment proof | Prove UPI transfers were legitimate |

| Property Documents | Asset proof | Explain large deposits from asset sales |

| Rental Agreement | Address and income proof | Establish residency and income |

| Police NOC / Court Order | Legal clearance | Required if freeze was legally initiated |

Bring originals and self-attested photocopies of everything.

Bank Account Frozen Due to Cybercrime Complaint

This is the scenario most people in India are facing in 2026.

Here is what typically happens:

A fraud victim — someone who lost money through UPI fraud, investment scam, or online shopping fraud — files a complaint on cybercrime.gov.in or calls 1930. The system or investigating officer traces the money trail. The fraud proceeds reached your account — whether you are the fraudster, an intermediary, or a completely innocent recipient.

The bank receives a direction to freeze the account and does so immediately, often without notifying you first.

Why innocent people get caught in this:

- You sold something online and the buyer paid with money obtained through fraud

- You did a crypto P2P trade and received INR from a fraud victim without knowing it

- You received a “payment” from a part-time job scheme that was actually a mule network

- Someone sent you money by mistake and that person was involved in fraud

What to do:

- Contact the cybercrime cell that filed the complaint — get contact details from the investigating officer at the police station

- Explain your transaction in detail

- Provide evidence that your receipt of funds was legitimate — chat records, invoices, platform screenshots

- Submit a detailed written representation to both the bank and the cybercrime cell

- If the amount is small and evidence is clear, many freezes resolve within weeks

- If the amount is large or the fraud trail is complex, expect a longer investigation

Timeline: Cybercrime freezes typically take 2 weeks to 6 months for innocent account holders. Cooperation and documentation quality are the biggest factors.

Bank Account Frozen After Receiving Fraudulent Funds

Even if you had absolutely no idea the funds you received were connected to fraud, your account can be frozen as part of the money trail investigation.

This is how fraud money typically moves:

Fraud victim → Fraudster’s mule account → Your account → Another account

Your account is in the middle of this chain. Even though you did nothing wrong, investigators must verify your role before releasing the freeze.

What innocent recipients should do:

- Do not attempt to transfer remaining funds out of your account — this looks suspicious and can worsen your situation

- Immediately document how you know the sender and why they sent you money

- Contact the sender and obtain their explanation in writing

- Submit all documentation to the bank and investigating authority

- If the sender was known to you legitimately (employer, client, family member), provide proof of that relationship

- Do not delete any messages, emails, or transaction records

Bank Account Frozen Due to Cryptocurrency Transactions

Crypto-related account freezes are among the most complex and fastest-growing category in India.

| Scenario | Risk Level | Possible Resolution |

| P2P trade: received INR from fraud victim | High | Provide P2P platform records, trade history, KYC |

| Transferred INR to exchange for crypto purchase | Medium | Provide exchange account details and purchase records |

| Received payment for legitimate crypto sale | Medium | Provide counterparty chat, trade records |

| Account linked to flagged exchange wallet | High | Blockchain trace report, legal representation |

| Received crypto mining proceeds | Low | Mining wallet records, hardware purchase proof |

| Involved in flagged DeFi transaction | Very High | Complex; requires specialist legal advice |

Key guidance for crypto-related freezes:

- Always use regulated, KYC-compliant exchanges registered with FIU-IND

- Maintain complete records of every P2P trade including counterparty details

- If trading P2P, use only platform escrow systems — never off-platform transfers

- When your bank account is frozen after a crypto transaction, provide full exchange KYC documentation, P2P trade screenshots, and chat records with the counterparty

- The Enforcement Directorate may be involved in large crypto-related freezes — this requires immediate legal representation

What Is a Mule Account?

A mule account is a bank account used to receive and transfer proceeds of crime, typically to help fraudsters move money while obscuring the original source.

How people become mule accounts unknowingly:

- They respond to a “part-time job” posting that pays them to receive payments and transfer them forward

- They rent their account to someone for “business purposes” in exchange for money

- A “friend” asks to use their account for a large transaction temporarily

- They are recruited through Telegram or WhatsApp to become “payment agents”

- They sell their old SIM card and the new user opens a bank account in their name

Warning signs that you may be being used as a mule:

- Someone asks to use your bank account for a fee or commission

- You are asked to receive payments and forward them minus a percentage

- A new online “employer” sends you money and asks you to buy gift cards or crypto

- You receive unexpected large deposits from strangers

- Someone sends you money and immediately asks you to send it somewhere else

Consequences:

Even unknowing mule account holders can face criminal charges under BNS provisions for fraud and PMLA provisions for money laundering. Cooperation with investigators, demonstrating lack of criminal intent, and providing full transparency are critical.

Rights of Account Holders

You have rights even when your account is frozen. Know them.

Right to information: You have the right to know why your account has been frozen. The bank must provide you with the reason and the reference details of the authority that directed the freeze, upon formal written request.

Right to be heard: In cases of police-initiated or cybercrime-initiated freezes, you have the right to present your side of the story to the investigating authority. Exercise this right promptly and in writing.

Right to legal representation: You can engage a lawyer at any stage — when dealing with the bank, the cybercrime cell, the police, or any court. Never waive this right.

Right to challenge unlawful freezes: If a freeze has been applied without legal authority, in violation of RBI guidelines, or without following due process, you can challenge it before the Banking Ombudsman, Consumer Forum, or the High Court.

Right to essential financial access: While there is no absolute right to access frozen funds during an investigation, courts have in several cases allowed limited access to accounts for basic necessities, salary payments, and essential business operations, especially when the account holder is demonstrably innocent.

Can You Use Money in a Frozen Account?

| Transaction Type | Full Freeze | Debit Freeze | Partial Freeze |

| Receiving salary credit | No | Yes | Depends |

| Receiving other incoming transfers | No | Yes | Depends |

| ATM cash withdrawal | No | No | Limited |

| UPI payments outward | No | No | Limited |

| UPI payments inward | No | Yes | Depends |

| Cheque clearance (outgoing) | No | No | Limited |

| Fixed deposit creation | No | No | No |

| Bill payments | No | No | Limited |

| Loan EMI debit | Usually blocked | Usually blocked | Depends |

Important: Even with a debit freeze, incoming credits continue. This means your salary, rental income, or other deposits may still arrive — but you cannot withdraw them until the freeze is lifted. This can create significant hardship.

If you are facing genuine hardship due to inability to access salary or essential funds, this fact should be specifically highlighted in your representation to the investigating authority and the bank. Courts have shown sensitivity to hardship cases.

How Long Does It Take to Unfreeze a Bank Account?

| Scenario | Estimated Time | Key Factors |

| KYC documentation update | 1–7 days | Speed of document submission |

| Bank’s internal fraud review (cleared) | 7–30 days | Cooperation with bank |

| Simple cybercrime freeze (innocent, clear evidence) | 2–8 weeks | Quality of documentation, authority response time |

| Complex cybercrime investigation | 3–12 months | Investigation complexity, number of parties |

| Police investigation freeze | 1–6 months | Investigation progress, chargesheet filing |

| Court order freeze | Until court order modified | Requires legal proceedings |

| ED/PMLA freeze | 6 months to years | Complexity of money laundering investigation |

| Wrongful freeze (contested legally) | 1–6 months | Strength of legal challenge |

Factors that extend timelines:

- Multiple parties involved in the fraud chain

- Funds crossed international boundaries

- Large amounts attracting serious investigation

- Delayed response from account holder

- Missing documentation

- Unresponsive investigating officers

Factors that shorten timelines:

- Immediate cooperation

- Complete documentation

- Clear paper trail of legitimate transactions

- Proactive engagement with investigators

- Legal representation

Common Mistakes That Delay Unfreezing

- Ignoring the freeze and hoping it resolves itself. Freezes do not resolve automatically. Every day without action is a day added to the freeze duration.

- Providing incomplete documents. Submitting half the required documents causes repeated requests and delays. Submit everything at once.

- Making verbal representations only. Everything must be in writing. Verbal assurances from bank staff carry no legal weight.

- Attempting to move funds immediately after a partial unfreeze. Moving money rapidly immediately after restrictions are eased triggers fresh suspicion.

- Arguing or being hostile with bank staff or police. Your attitude significantly affects how investigators and bank officers handle your case.

- Hiding information about the disputed transaction. Investigators will eventually find out. Concealment transforms a freeze into a criminal investigation.

- Trusting intermediaries who promise to unfreeze accounts for a fee. These are scammers. Nobody can “fix” a legitimate investigation for a fee.

- Opening a new account at the same bank. The bank will link accounts. Opening new accounts while under investigation raises additional red flags.

- Not informing your employer. If your salary account is frozen, your employer needs to know to arrange alternative payment. Do not let salary payments bounce.

- Not reading and responding to notices within deadlines. Missed deadlines can result in your freeze converting to a legal seizure.

- Failing to engage a lawyer for court-ordered freezes. Court orders can only be challenged through proper legal proceedings.

- Assuming the bank controls the freeze. If the freeze is ordered by police or court, the bank cannot lift it independently. Going only to the bank wastes time.

- Not keeping copies of every document submitted. Banks and authorities sometimes lose documents. Always keep duplicates.

- Refusing to cooperate with the investigating officer. Non-cooperation is interpreted as guilt. Cooperate fully while being aware of your rights.

- Sending money from another account to the frozen account. This increases the amount under investigation without resolving anything.

- Discussing the freeze on social media. Publicizing the investigation can complicate legal proceedings and attract unwanted attention.

- Contacting wrong branch or wrong authority. Only your home branch can act on your account. Only the specific authority that initiated the freeze can release it.

- Waiting too long to engage legal help. Early legal advice can dramatically shorten resolution timelines.

- Providing false information in your representation. Even well-intentioned embellishment constitutes a false statement to authorities.

- Not following up after submitting documents. Submission is step one. Follow up in writing every 7–10 days.

Real-Life Scenarios

Case Study 1: UPI Fraud Investigation

What happened: Meera, a homemaker in Hyderabad, sold handmade items through Instagram. A buyer transferred ₹18,000 via UPI and collected the goods. Three weeks later, Meera’s bank account was frozen. The buyer had funded the UPI transfer using a credit card obtained through identity theft.

Why freeze occurred: The identity theft victim filed a cybercrime complaint. The trail led to the buyer’s account, then to Meera’s account.

Resolution process: Meera visited her branch and obtained the cybercrime case number. She contacted the Hyderabad cyber cell with all Instagram order records, delivery proof, and conversation history with the buyer. She submitted a written explanation showing she was a legitimate seller with no knowledge of fraud.

Outcome: Freeze lifted in 6 weeks. The investigating officer confirmed she was a victim of a fraudulent buyer.

Lessons: Maintain all records of online sales — screenshots of orders, delivery proof, and customer communication. These are critical if your account is ever questioned.

Case Study 2: Crypto P2P Transaction

What happened: Rajan, a 27-year-old software engineer in Bengaluru, regularly traded crypto on a P2P platform. He sold USDT worth ₹2.8 lakh to a buyer through the platform’s escrow. The INR was deposited to his bank account. Unknown to Rajan, the buyer had funded that purchase with money from a fraud victim. His account was frozen by the Karnataka Cyber Cell.

Why freeze occurred: The fraud victim had filed a cybercrime complaint. Blockchain investigation traced the USDT to the fraud victim’s crypto account. The INR trail led to Rajan’s account.

Resolution process: Rajan engaged a cyber law advocate. Together they compiled complete P2P trade records from the platform, the KYC-verified counterparty details, the platform’s transaction confirmation, and evidence that the trade was conducted through the platform’s official escrow system.

Outcome: Freeze lifted in 3.5 months. Rajan was not charged. The actual fraudster was separately identified.

Lessons: Always trade through regulated platforms. Never do off-platform P2P transfers. Maintain complete records of every crypto trade.

Case Study 3: Salary Account Freeze

What happened: Vikram, a government contractor in Delhi, received payment from a client for services rendered. The client’s account had been flagged in a broader fraud investigation. Vikram’s account — his primary salary account — was frozen.

Why freeze occurred: His account received funds from a flagged account, placing it in the fraud money trail automatically.

Resolution process: Vikram submitted his service agreement, GST invoices, and delivery proof demonstrating the payment was for legitimate services. His chartered accountant prepared a detailed financial explanation. His employer provided a letter confirming his employment and the account’s use as a salary account.

Outcome: Partial unfreeze within 45 days allowing salary credits. Full unfreeze in 4 months.

Lessons: Business accounts should always have proper documentation for every large transaction — contracts, invoices, and delivery records.

Case Study 4: Small Business Owner

What happened: Priya ran a small export business. Her current account showed multiple large incoming SWIFT transfers from overseas clients and multiple outgoing transfers to suppliers. The bank’s AML system flagged the pattern as potential money laundering and froze the account.

Why freeze occurred: Rapid inflow-outflow patterns consistent with layering triggered AML flags without any external fraud complaint.

Resolution process: Priya visited the bank with her export documentation, FIRC (Foreign Inward Remittance Certificates) for all overseas receipts, supplier invoices for outgoing payments, GST returns, and bank statements from previous years showing the same normal business pattern.

Outcome: Bank-initiated review completed in 18 days. Account unfrozen.

Lessons: Businesses with high transaction volumes should proactively maintain a relationship with their bank relationship manager and provide annual documentation of their business model and transaction patterns.

Case Study 5: Wrongful Freeze

What happened: Suresh from Pune found his account frozen due to a clerical error — the police had submitted the wrong account number in their freeze direction. The account that should have been frozen belonged to someone with a similar name.

Why freeze occurred: Purely administrative error. Suresh had no connection to any fraud whatsoever.

Resolution process: The bank confirmed the freeze was based on a police direction but could not release it without police authorization. Suresh’s lawyer filed a representation directly with the relevant police station. The IO (Investigating Officer) reviewed the direction and confirmed the error.

Outcome: Freeze lifted in 12 days once the police confirmed the error in writing to the bank.

Lessons: Even wrongful freezes must go through the initiating authority for resolution. Engaging a lawyer immediately in such cases is the fastest path to resolution.

Legal Remedies if the Freeze Continues

If normal channels have not resolved the freeze after a reasonable period, you have formal legal options.

Representation to Senior Authorities

Write formally to the Superintendent of Cyber Crime Police, the Deputy Commissioner of Police (Economic Offences), or equivalent senior officers. Attach all documentation. This often resolves cases stuck at lower levels.

Banking Ombudsman (RBI)

If the freeze is bank-initiated (not police or court) and the bank has not responded adequately within 30 days of your written complaint, you can file a complaint with the RBI’s Banking Ombudsman. The Ombudsman can direct the bank to provide reasons, resolve KYC issues, and compensate for wrongful freeze. File at bankingombudsman.rbi.org.in.

Limitation: The Banking Ombudsman cannot intervene in police or court-ordered freezes.

Consumer Forum

Under the Consumer Protection Act, 2019, deficiency in banking services — including wrongful or poorly communicated account freezes — can be challenged at the District Consumer Disputes Redressal Commission.

Writ Petition to High Court

When all other avenues fail — particularly for police or court-ordered freezes that are taking unreasonably long or lack proper legal basis — a Writ Petition under Article 226 of the Constitution can be filed before the relevant High Court.

Courts have in many cases directed:

- Release of frozen funds for essential expenses

- Time-bound completion of investigations

- Full lifting of freezes where no criminal nexus is established

- Compensation for wrongful freezes

This route requires a lawyer and involves legal costs, but is effective especially when the freeze amount is significant.

How to Prevent Future Account Freezes: 25 Practical Tips

- Complete and update your bank KYC documentation every time your address, phone, or name changes.

- Maintain 12 months of bank statements readily available at all times.

- File Income Tax Returns every year, even if below the taxable threshold.

- Keep all invoices, receipts, and contracts for every significant transaction you make.

- Never accept payments from strangers without knowing the source and purpose.

- Never rent, lend, or share your bank account with anyone for any reason.

- Do not allow others to use your phone for banking even temporarily.

- If selling on platforms like OLX, Meesho, or Instagram, keep full chat records and delivery proof.

- Use only FIU-IND registered crypto exchanges for all crypto transactions.

- Always use platform escrow for P2P crypto trades — never transfer outside the platform.

- Maintain P2P trade records including counterparty KYC screenshots.

- Verify the identity of anyone who sends you large payments — especially new contacts.

- Avoid receiving payments from multiple unknown sources in the same time period.

- Be extremely cautious of online job offers that involve receiving and forwarding payments.

- Never participate in schemes where you are paid to receive and transfer money.

- Report suspicious contacts or payment requests to your bank’s fraud team proactively.

- Keep a dedicated business account if you run a business — do not mix personal and business transactions.

- For high-value transactions, document the purpose in writing before the transaction.

- If you receive an unexpected large deposit, contact your bank immediately to clarify.

- Keep your mobile number and email registered with the bank current for instant alerts.

- Enable transaction alerts for every debit and credit on your account.

- Regularly review your bank statement for any transactions you do not recognize.

- Maintain your relationship with your bank’s branch manager — familiarity helps in dispute resolution.

- If your documents or SIM card are ever lost or stolen, report to bank immediately.

- Educate family members about the risks of account sharing, mule account schemes, and online job frauds.

Expert Analysis: Why More Accounts Are Being Frozen in India

The number of bank account freezes in India has increased dramatically over the past three years. Understanding why this is happening helps account holders protect themselves.

UPI has transformed the fraud landscape. India processes billions of UPI transactions monthly. The speed that makes UPI convenient also makes it attractive for fraud. When fraud happens at UPI scale, the reporting and investigation process moves fast — and accounts get frozen before full investigation is possible.

The 1930 helpline and cybercrime portal have been highly effective. These systems have made fraud reporting fast and accessible. Millions of complaints are filed annually. Each complaint triggers an automated or manual freeze direction. The scale of fraud reporting means more accounts are swept into investigations, including innocent ones.

AML compliance requirements have become more stringent. RBI’s updated AML guidelines require banks to proactively monitor and flag suspicious patterns. Banks that fail to comply face regulatory action. This creates an incentive to freeze first and investigate later.

Crypto’s growth has created new freeze triggers. India’s crypto trading volume is significant. P2P trading in particular creates complex money trails that intersect with traditional banking, triggering freezes at the banking layer even when the crypto transaction itself was legitimate.

Mule account networks have become sophisticated. Organized crime groups actively recruit account holders — particularly through fake job advertisements. When these mule networks are disrupted, dozens or hundreds of accounts are frozen simultaneously in coordinated police operations.

The net effect is that more innocent people are caught in investigation sweeps. The system is improving — cybercrime cells are becoming more sophisticated and quicker at exonerating innocent parties — but it is not yet fast enough to prevent significant hardship for affected account holders.

Frequently Asked Questions

Q1. Can police freeze a bank account without a court order? Yes. Under Section 102 of the CrPC (now corresponding provisions of BNSS, 2023), a police officer investigating a cognizable offence can seize property — including bank accounts — if they believe the property may be connected to a crime. The officer must report the seizure to a Magistrate, but prior court approval is not required. Additionally, banks receive informal freeze directions from police stations regularly. While informal directions do not have the same legal authority as formal Section 102 orders, banks often comply as a precaution. If you believe your account was frozen without legal basis, this can be challenged before a Magistrate or High Court.

Q2. Can a bank freeze my salary account? Yes. Banks can freeze any account — including salary accounts — when directed by investigating authorities or when their own compliance systems flag the account. There is no legal exemption for salary accounts. However, if your salary account is frozen and you can demonstrate genuine financial hardship, you can petition the investigating authority or court to allow limited access for essential living expenses. In several High Court decisions, courts have ordered partial access to frozen salary accounts for individuals with no criminal nexus.

Q3. Can I receive money in a frozen account? It depends on the type of freeze. A full freeze blocks both incoming and outgoing transactions — you cannot receive any credits. A debit freeze — the most common type in fraud investigations — allows incoming credits but blocks outgoing transactions. So your salary, rental income, or other deposits may still land in your account, but you cannot withdraw them. Check with your bank to determine which type of freeze has been applied to your account.

Q4. Can I open another bank account while my existing one is frozen? Generally yes — having one frozen account does not legally prevent you from opening another account at a different bank. However, some banking systems may flag your name or PAN if you are under active investigation, potentially causing the new account application to be scrutinized or rejected. If the freeze is part of a broader criminal investigation or court order, consult a lawyer before opening new accounts to ensure this does not create complications in your case.

Q5. What is a debit freeze exactly? A debit freeze is a restriction that prevents you from making any withdrawals, transfers, or payments from your account. Money can still be deposited into the account, but you cannot take it out. This is the most common type of freeze applied in cybercrime and fraud investigations. The bank preserves the funds in your account pending investigation. If you are cleared, the freeze is lifted and you regain full access. If you are found to have received fraud proceeds, the funds may be transferred to the victim or court as ordered.

Q6. How do I contact cybercrime authorities about my frozen account? First, visit your nearest police station and ask which cybercrime cell is handling your case — get the station name, case number, and the IO’s contact. Then contact that cybercrime cell directly by visiting in person and submitting a written representation. You can also email the State Cyber Crime Department. The national helpline is 1930. State cyber crime cells maintain websites and email contacts — search for your state’s cyber crime cell contact details. Always follow up every communication in writing and keep copies.

Q7. Can crypto transactions trigger a bank account freeze? Absolutely yes, and this is increasingly common. If you receive INR in your bank account from someone who funded the transfer using cryptocurrency obtained through fraud, your account may be frozen as part of the money trail. This is most common in P2P crypto trading. Additionally, if you transfer INR to a crypto exchange and that exchange is linked to flagged transactions, your account may be investigated. Using only FIU-IND registered exchanges and maintaining complete trade records significantly reduces this risk.

Q8. How long does a cybercrime investigation-related freeze typically last? For innocent account holders who cooperate fully and provide complete documentation, cybercrime freezes often resolve in 4–12 weeks. For complex cases involving large amounts, multiple parties, or offshore elements, investigations can take 3–12 months or longer. The single biggest factor within your control is how quickly and completely you respond to authorities. Delays in providing documents or responding to notices directly extend the freeze duration.

Q9. What if I am completely innocent but my account is frozen? Being innocent does not automatically resolve a freeze — you must actively demonstrate your innocence. File a detailed written representation with the investigating authority, supported by complete documentation of every transaction in question. Engage a lawyer to assist in this process. If the investigating authority does not act within a reasonable time, escalate to senior officers or approach the High Court via Writ Petition. Courts have consistently protected innocent account holders and ordered time-bound investigations. Document every step of your cooperation for future legal use.

Q10. Can I withdraw cash from my frozen account? No. If your account has a debit freeze or full freeze, ATM withdrawals are blocked. This is one of the most immediate hardships victims experience. If you are facing a genuine emergency — medical expenses, for example — inform the investigating authority and your bank in writing and request emergency partial access. Some banks and authorities can arrange limited access in genuine humanitarian cases, though this is not guaranteed.

Q11. Can a bank account freeze be challenged legally? Yes. Freezes applied without proper legal authority, without following RBI guidelines, or continuing beyond reasonable investigation timelines can be challenged. The available legal avenues include: written representation to the bank and investigating authority; Banking Ombudsman (for bank-initiated freezes); Consumer Forum; and Writ Petition before the relevant High Court. Courts have successfully ordered lift of freezes in cases involving wrongful freezes, disproportionate freeze durations, and clear absence of criminal nexus.

Q12. What happens if I ignore my frozen account? Ignoring a frozen account is one of the worst things you can do. Investigations may proceed in your absence, resulting in a chargesheet or adverse order without your input. Notices you do not respond to may be deemed served, allowing proceedings to continue against you. The freeze may become a permanent seizure. And delays in responding will extend the freeze duration significantly. Engage with the situation immediately regardless of whether you believe you are innocent.

Q13. Will my credit score be affected by a frozen account? Not directly — a frozen bank account does not in itself affect your CIBIL score. However, if EMI payments or other financial commitments that are debited from the frozen account are missed due to the freeze, those missed payments will affect your credit score. Inform lenders proactively if your frozen account is linked to loan repayments and arrange alternative payment methods while the freeze is active.

Q14. Can the ED freeze my account for crypto transactions? Yes. The Enforcement Directorate has authority under PMLA to investigate and freeze accounts suspected of being used in money laundering. Large crypto-related transactions — particularly if they involve foreign exchanges, large amounts, or complex transaction chains — can attract ED investigation. ED-initiated freezes are among the most serious and complex to resolve, typically requiring experienced legal representation.

Q15. What if the fraud amount in my account is very small? Even small amounts can trigger freezes. However, smaller amounts often resolve faster — investigating authorities typically prioritize cases based on amount and complexity. A clear explanation and documentation for a small disputed transaction can sometimes resolve a freeze within 2–4 weeks. Do not assume a small amount means no action is needed — file your representation promptly regardless.

Q16. Can the bank permanently seize my funds? Banks cannot permanently seize funds on their own authority. However, if criminal proceedings result in a court order directing that funds be transferred to the victim or government, funds can be permanently removed from your account through that judicial process. This is why engaging in the investigation process is so important — your representation and evidence determine whether your funds are ultimately returned.

Q17. Is there a time limit on how long a bank account can remain frozen? There is no single statutory maximum duration. However, courts have recognized that indefinite freezes without progress violate the account holder’s rights. In cases where investigations have stalled or no chargesheet has been filed within the limitation period, account holders have successfully petitioned High Courts to order the release of frozen funds. If your account has been frozen for more than 6 months without clear investigation progress, consult a lawyer about your options.

Q18. Can my joint account holder access a frozen joint account? No. A freeze on a joint account restricts all account holders from accessing funds, regardless of who triggered the investigation. Both/all joint account holders are equally affected. All account holders should cooperate with the investigation.

Q19. Can I file a complaint against the bank for freezing my account wrongfully? Yes. If the bank applied or maintained a freeze without legal basis, did not inform you of the reason within a reasonable time, or acted contrary to RBI guidelines, you can file a complaint with the Banking Ombudsman. If you suffered financial loss due to a wrongful bank-initiated freeze, you may also be able to claim compensation through the Consumer Forum.

Q20. What should I do if I suspect I was used as a mule account without my knowledge? Report it proactively — to your bank immediately and to the cybercrime portal. Explain that you believe your account was used without your knowledge or through deception. Provide all evidence supporting your lack of knowledge. Proactive disclosure demonstrates good faith and is treated very differently by investigators than discovered participation. Early self-reporting can be the difference between victim status and suspect status.

Q21. Can a freeze be lifted the same day? In exceptional circumstances — particularly clear clerical errors or cases where all required documentation is already available — same-day resolution is possible. For KYC freezes with complete documents, 1–3 days is achievable. For most fraud investigation freezes, same-day resolution is not realistic. Set accurate expectations and focus on making your process as complete and fast as possible.

Q22. What if the bank says they cannot tell me why my account is frozen? Banks sometimes cite investigation confidentiality. However, you have a right to know at minimum that your account is restricted and the general nature of the restriction. Submit a written request to the Branch Manager demanding the reason in writing. If refused, escalate to the Banking Ombudsman. Courts have repeatedly held that account holders are entitled to reasons for restrictions on their accounts.

Q23. Can a government employee’s account be frozen? Yes. Government employment provides no exemption from account freeze in fraud investigations. However, the consequences — inability to draw salary — are treated seriously by courts and investigating authorities. If you are a government employee facing account freeze, include your employment details prominently in your representation and request expedited review.

Q24. What if the fraud amount is more than what is in my account? If the fraud amount claimed exceeds your account balance, the investigating authority may freeze your account and potentially pursue additional legal action to attach other assets. This is a serious situation requiring immediate legal representation. Do not wait.

Q25. Can I get a temporary stay on a bank account freeze? Yes. High Courts can grant interim stay orders on account freezes pending hearing of a Writ Petition. If your account freeze is causing severe financial hardship and the freeze appears to lack legal basis or is disproportionate, a lawyer can apply for urgent interim relief. Courts have granted stays pending full hearing in several cases.

Conclusion

A frozen bank account is frightening — but it is not the end of the road.

Why accounts get frozen: The rise of digital payments, cybercrime reporting systems, and AML compliance requirements means more accounts are being swept into fraud investigations — including accounts belonging to completely innocent people.

What to do immediately:

- Call 1930 and file at cybercrime.gov.in if relevant

- Visit your home branch — get the freeze reason in writing

- Preserve all transaction records, chat histories, and receipts

- Contact the investigating authority directly and cooperate

- Engage a lawyer if the freeze involves police, courts, or ED

- Follow up every 7–10 days in writing

Realistic expectations:

- Bank-initiated KYC freezes: days to weeks

- Cybercrime freezes for clearly innocent parties: weeks to months

- Complex investigation freezes: months to years

Preventing future freezes:

Never share or rent your account. Maintain complete records of all transactions. Use only regulated platforms for crypto. Verify the source and purpose of unexpected large payments. Keep your KYC current.

You have rights. You have legal remedies. And the system — imperfect as it is — does distinguish between fraudsters and innocent victims. Cooperation, documentation, and timely action are your most powerful tools.

Do not wait. Act today.

Legal Disclaimer: This article provides general educational information for Indian bank account holders and does not constitute legal advice. Laws, regulations, and procedures may change. Every situation is unique. Please consult a qualified lawyer for advice specific to your case. The author and publisher accept no liability for actions taken on the basis of this article.

my bank account blocked or frozen please un freeze

Please fill our contact form and one of our representative will help you out with the issue – https://www.nahar.om/contact