India’s digital payments boom has brought convenience to hundreds of millions — but also a sharp rise in card fraud. If you’ve ever spotted an unauthorized debit on your account, the chargeback process is your legal right to fight back. This guide covers everything: what chargebacks are, how to file one, RBI protections, timelines, and what to do if your bank says no.

What Is a Chargeback in Banking?

A chargeback is a forced reversal of a card transaction, initiated by your issuing bank on your behalf. Unlike a merchant refund — which depends on the seller’s cooperation — a chargeback goes through the card network (Visa, Mastercard, RuPay) directly to the merchant’s bank, compelling them to return your money.

The Reserve Bank of India (RBI), through its 2017 circular “Customer Protection – Limiting Liability of Customers in Unauthorized Electronic Banking Transactions,” has made this a legal right, not merely a banking courtesy. Once you report fraud promptly, your liability can be zero.

Quick Answer: A chargeback is a bank-initiated payment reversal for unauthorized, fraudulent, or unfulfilled card transactions. It is backed by RBI guidelines and can result in full recovery if reported within 3 working days.

Common Situations Where You Can File a Chargeback

| Situation | What Qualifies |

|---|---|

| Unauthorized Card Usage | Card stolen, skimmed, or details phished and used without your consent |

| Online Shopping Scams | Paid for goods that never arrived, were counterfeit, or misrepresented |

| Failed ATM Withdrawal | ATM didn’t dispense cash but your account was debited |

| Duplicate Transactions | Charged twice for a single purchase due to a POS or gateway glitch |

| Subscription Billing Fraud | Charged for a cancelled subscription or unauthorized recurring billing |

Credit Card vs Debit Card Chargeback in India

| Feature | Credit Card | Debit Card |

|---|---|---|

| Fund Impact | Affects credit limit; your cash is untouched | Money leaves your account immediately |

| Ease of Recovery | Higher — bank has vested interest (it’s their credit) | Moderate — bank recovers your funds from the merchant |

| Provisional Credit | Often within 7–10 working days | Similar, but liquidity impact is felt sooner |

| Consumer Protection | Stronger zero-liability framework | Covered under RBI rules; requires faster reporting |

| Dispute Window | Up to 60–120 days (network-dependent) | Prompt reporting critical; same RBI timelines apply |

Key takeaway: Credit cards generally offer a smoother chargeback experience because your own money isn’t immediately at stake. For debit cards, acting within 24–48 hours is even more critical.

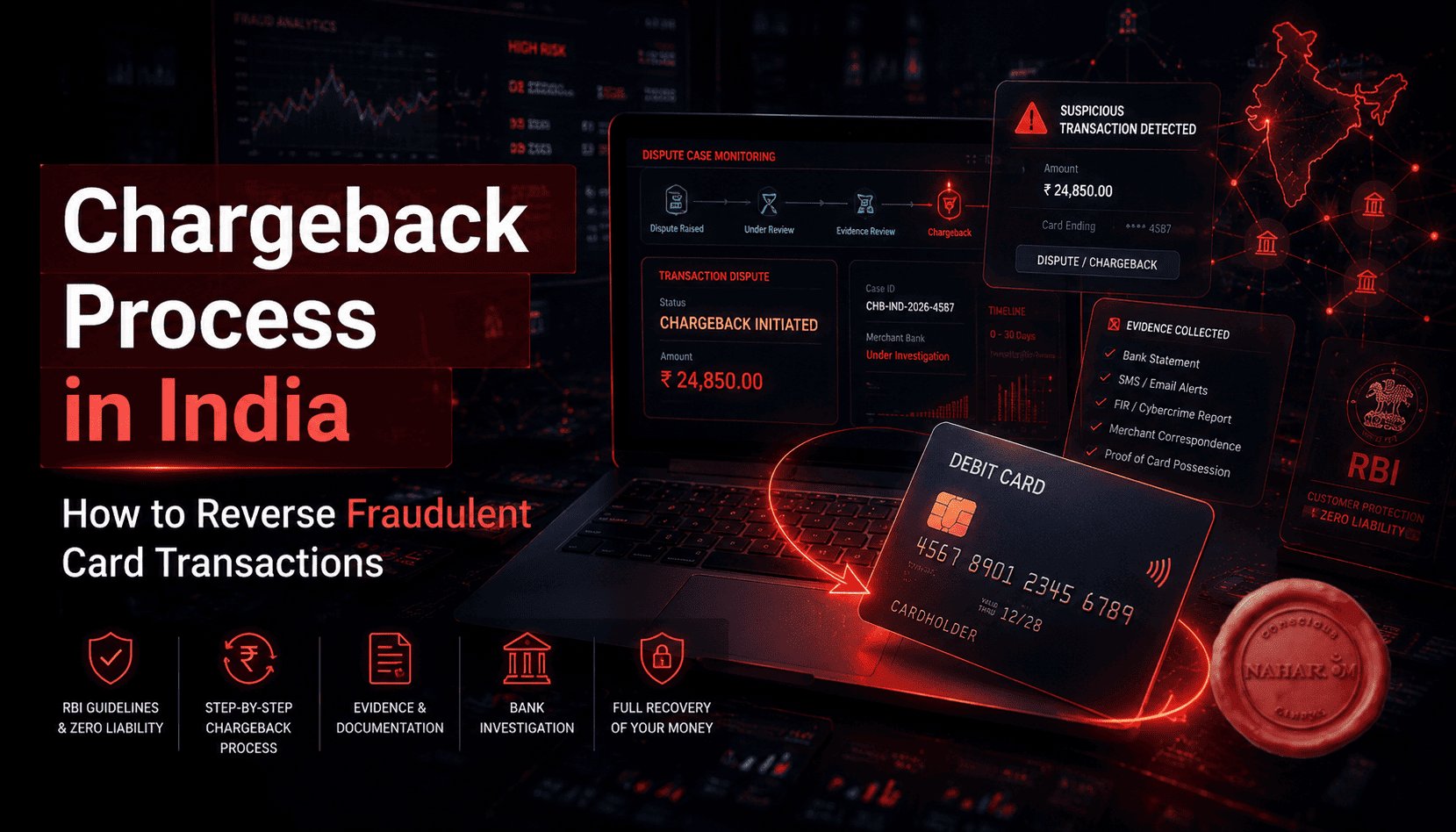

Step-by-Step Chargeback Process in India

Step 1 — Block the Card Immediately

Use your bank’s mobile app, internet banking, or 24/7 helpline to freeze or block the card the moment you spot a suspicious transaction. Also disable international and online transactions as an extra layer of protection.

Step 2 — Formally Inform the Bank

Call customer care and report it as fraud or unauthorized. Note down the Service Request (SR) number — this reference is essential for tracking and escalation. Follow up with an email to the bank’s fraud/dispute department for a written record.

Step 3 — Raise a Dispute Request

Fill out the bank’s Cardholder Dispute Form (CDF) or Transaction Dispute Form, available on the bank’s app, net banking portal (Cards > Transaction Dispute > Fraudulent/Unauthorised), or at a branch. Specify the transaction date, amount, merchant name, and reason code.

Step 4 — Submit Supporting Evidence

Strong documentation is your most powerful tool. Submit:

- Bank statement with the disputed transaction highlighted

- Screenshots of SMS/email transaction alerts (timestamped)

- FIR or cybercrime complaint acknowledgement from cybercrime.gov.in

- Email correspondence with the merchant (for non-delivery disputes)

- Proof of card possession at the time of the disputed transaction

Step 5 — Bank Investigation

Your issuing bank forwards the dispute to the merchant’s bank via the card network. The merchant is typically given 14–30 days to submit “compelling evidence” (signed receipt, delivery proof, OTP logs). Many banks issue a provisional/shadow credit of the disputed amount during this window if your initial case is strong.

Step 6 — Final Settlement

If the merchant cannot prove transaction legitimacy, the chargeback is confirmed and your provisional credit becomes permanent. If the merchant provides valid counter-evidence, the provisional credit is reversed. The entire process must conclude within 90 days under RBI mandate.

Documents Required for a Chargeback Claim

| Document | Why It Matters |

|---|---|

| Bank/Card Statement | Establishes date, amount, and payee of the disputed transaction |

| Transaction Screenshot | Clean digital record from your bank app or net banking portal |

| SMS/Email Alerts | Timestamped proof you received notification of the transaction |

| FIR / Cybercrime Complaint | Official acknowledgement from cybercrime.gov.in or local police; makes banks treat the case as a reported crime |

| Merchant Correspondence | Emails or chat transcripts of refund requests or delivery failures |

For amounts above ₹5,000, most Indian banks strongly expect at least a cybercrime complaint acknowledgement from the National Cyber Crime Reporting Portal.

RBI Guidelines for Unauthorized Transactions

Zero Liability Conditions

You bear no financial loss under either of these conditions:

- Bank’s fault: Fraud due to the bank’s own negligence, system failure, or security deficiency — zero liability regardless of when you report.

- Third-party breach: Fraud by an external party where neither you nor the bank is responsible — zero liability if reported within 3 working days.

Liability Based on Reporting Timeline (Third-Party Breach)

| When You Report | Your Maximum Liability |

|---|---|

| Within 3 working days | ₹0 (Zero Liability) |

| 4 to 7 working days | Up to ₹5,000–₹25,000 (varies by account/card type) |

| Beyond 7 working days | As per the bank’s board-approved policy; may be full liability |

The clock starts from the day you receive the transaction alert (SMS or email), not from when you discover the fraud later.

When You Are at Fault

If you shared an OTP, PIN, or card credentials — even under social engineering — the bank considers this gross negligence. In that case, you bear the full loss until the point you report it. Any further transactions after reporting become the bank’s responsibility.

How Long Does a Chargeback Take in India?

- Provisional credit: Within 10 working days of filing the complaint (RBI-mandated, subject to initial investigation)

- Full investigation and final settlement: Up to 90 days

- Visa/Mastercard dispute window: Up to 120 days if the merchant raises a re-presentment (counter-dispute)

- Average resolution for genuine claims reported within 3 days: 12–22 days at major banks (HDFC Bank and Kotak report ~98% success rates; SBI Card and ICICI Bank above 94%)

Delays are most commonly caused by missing documentation, slow merchant response, or a complex cross-border transaction.

Why Chargeback Requests Get Rejected

| Reason | How to Avoid It |

|---|---|

| Late Reporting | Report within 24 hours; never wait beyond 3 days for zero liability |

| Weak Documentation | File a cybercrime complaint, gather all SMS/screenshots before submitting |

| Shared OTP or PIN | Never share credentials; banks treat this as gross negligence and reject claims |

| Merchant Provides Counter-Evidence | Collect your own evidence (non-receipt proof, location alibi) before the bank investigates |

| Friendly Fraud Detection | Banks track device/IP data; claims where a family member used the card are often flagged |

| Wrong Dispute Reason Code | Match your reason to the correct category (fraud vs. non-delivery vs. duplicate) |

What to Do if Your Bank Rejects the Chargeback

Rejection is not the end. You have a clear three-step escalation path:

1. Principal Nodal Officer (PNO) Every bank has a designated nodal officer for grievance redressal. Escalate formally in writing, asking for a detailed explanation of the rejection and the evidence used. This step is mandatory before approaching the RBI.

2. RBI Banking Ombudsman If the bank hasn’t resolved your complaint within 30 days, or has given an unsatisfactory response, file online at cms.rbi.org.in. You’ll need your bank complaint reference number. The Ombudsman can direct reversal and award compensation — and this service is completely free.

3. Consumer Court For larger amounts, approach the District Consumer Disputes Redressal Forum for “Deficiency in Service.” Consult a lawyer for claims above ₹20 lakh. This is typically used after exhausting the above channels.

Tips to Maximize Your Chargeback Success

- Act within 24 hours — Recovery probability drops sharply after the first day. The 3-day RBI window is a ceiling, not a target.

- File a cybercrime report simultaneously — Visit cybercrime.gov.in the same day. Banks escalate “reported crime” cases faster than standalone complaints.

- Keep communication factual — Quote RBI circular references, transaction dates, and SR numbers. Avoid emotional language.

- Always get an SR number — Every interaction with the bank should produce a Service Request number. This is your paper trail.

- Monitor your CIBIL score — For credit card disputes, ask the bank to mark the amount as “Disputed” so it doesn’t impact your credit score during the investigation.

- Don’t settle verbally — Always follow up phone calls with an email summarizing what was discussed.

Frequently Asked Questions

What is a chargeback and how does it work in India? A chargeback is a bank-initiated reversal of a disputed card transaction. You report the unauthorized or fraudulent charge to your issuing bank, which then contacts the merchant’s bank via the card network (Visa, Mastercard, RuPay) to claw back the funds. It is governed by RBI guidelines and can result in zero liability if reported within 3 working days.

How long does a chargeback take in India? Banks must provide provisional credit within 10 working days and resolve the case within 90 days under RBI rules. For genuine fraud cases reported quickly, major banks typically resolve claims in 12–22 days.

Can I file a chargeback on a debit card in India? Yes. Both credit and debit cards are covered under RBI’s chargeback framework. Debit card chargebacks follow the same steps, but since money leaves your account immediately, prompt reporting is even more critical.

Is an FIR mandatory to file a chargeback? No, an FIR is not mandatory to initiate a chargeback. However, an online cybercrime complaint from cybercrime.gov.in is strongly recommended and required by most banks for amounts above ₹5,000. It significantly strengthens your claim and is treated as official documentation of a reported crime.

What happens if I shared my OTP and got defrauded? Sharing an OTP is classified as gross negligence under RBI guidelines. The bank will likely reject the chargeback for the transaction itself. However, you should still report immediately — any further unauthorized transactions after the point of reporting become the bank’s responsibility.

Can UPI transactions be reversed through a chargeback? UPI does not have a formal chargeback system like card networks. You can raise a dispute through your bank or UPI app (BHIM, Google Pay, PhonePe), but recovery is significantly harder since transfers are instant. Report immediately to your bank to attempt freezing the recipient account, and file a complaint at cybercrime.gov.in.

What is the RBI zero liability rule for card fraud? Under RBI’s 2017 circular, if card fraud occurs due to a third-party breach (not your negligence) and you report it within 3 working days of receiving the transaction alert, you bear zero financial liability. If the fraud is due to the bank’s own negligence, you have zero liability regardless of when you report.

What should I do if my chargeback is rejected by the bank? Escalate to the bank’s Principal Nodal Officer first. If unresolved after 30 days, file a complaint with the RBI Banking Ombudsman at cms.rbi.org.in (free service). As a last resort, approach the District Consumer Court for deficiency in service.

How long do I have to file a chargeback in India? While Visa and Mastercard allow dispute windows of up to 120 days from the transaction date, RBI guidelines strongly incentivize reporting within 3 working days for zero liability. The practical advice: report the same day you spot an unauthorized transaction.

Can I dispute an international card transaction from India? Yes. Indian banks can raise chargebacks for international transactions through Visa or Mastercard’s global dispute resolution process. These cases may take longer due to cross-border coordination, but the same RBI customer liability rules apply on the Indian side.

Conclusion

Unauthorized card transactions are alarming, but India’s chargeback framework — backed by the RBI — gives you a legitimate, structured path to recovery. The single most important factor is speed: report within 3 working days, block the card immediately, file a cybercrime complaint on the same day, and maintain a paper trail of every interaction.

If your bank resists, you have the RBI Banking Ombudsman and consumer courts in your corner. With the right documentation and timely action, recovering your money is not just possible — it’s the expected outcome.

Block. Report. Dispute. Escalate if needed.

This article is for informational purposes only and does not constitute legal or financial advice. RBI guidelines are subject to updates; always verify with your bank or RBI’s official website (rbi.org.in) for the latest rules.