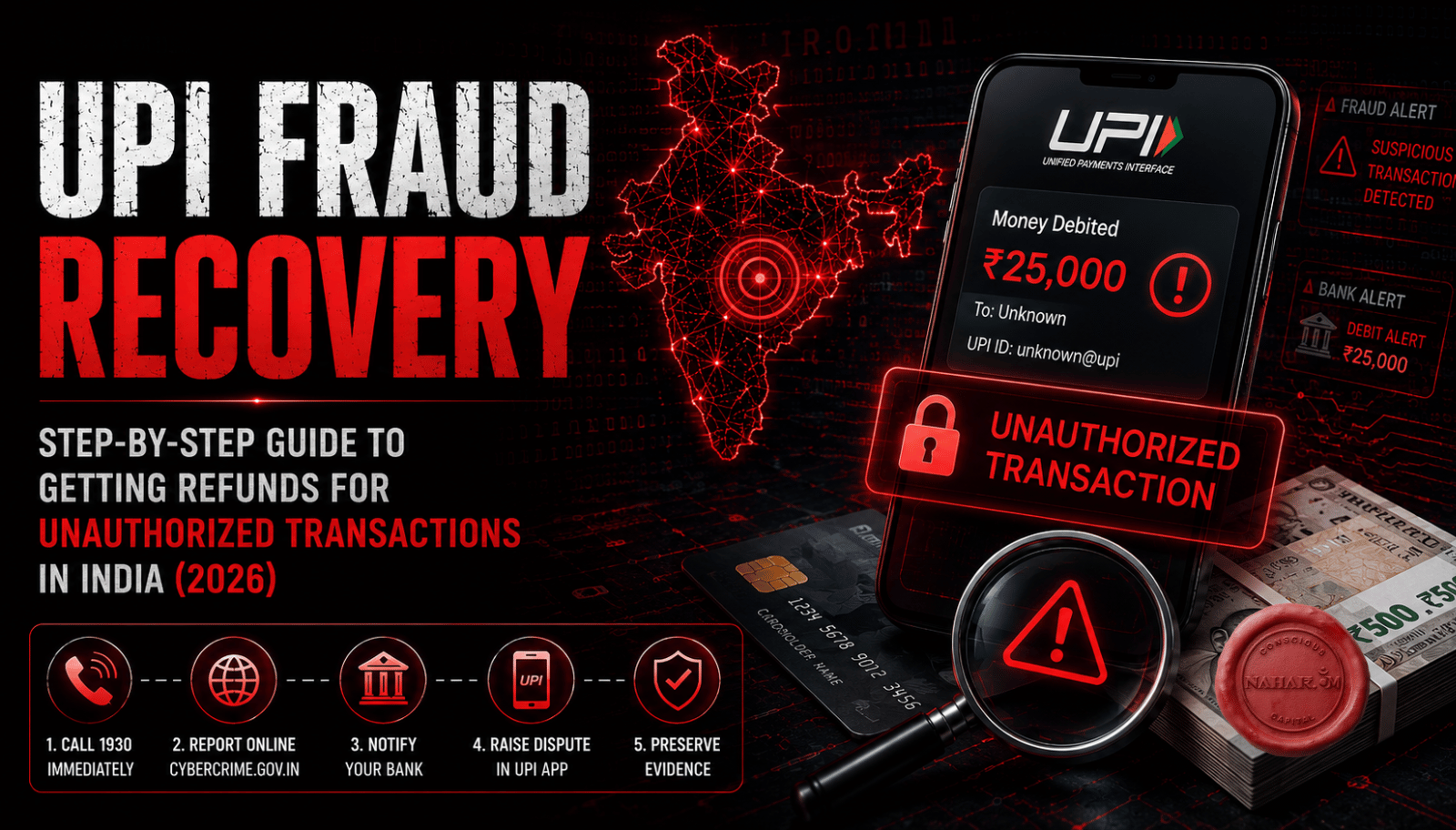

You can sometimes recover money lost in a UPI fraud, but recovery depends heavily on how fast you report it, what kind of fraud happened, and whether the funds can still be traced or frozen. The most important first steps are to call 1930, report the case on the National Cyber Crime Reporting Portal, inform your bank and UPI app immediately, and preserve all evidence such as the UTR, screenshots, SMS alerts, and scammer details.[i4c.mha.gov]

Expert review note: This guide is based on publicly available RBI guidelines, NPCI dispute mechanisms, banking complaint procedures, and cybercrime reporting frameworks. Rules, app flows, and dispute timelines may change, so users should always verify the latest steps on official bank, RBI, NPCI, app, and cybercrime portals before acting.[support.google]

Table of Contents

Introduction

You receive a call claiming to be from your bank. The caller says your account will be blocked unless you “verify” your UPI details right now. A few minutes later, ₹25,000 disappears from your account through a UPI transaction you never intended to approve.

This is exactly how many UPI frauds unfold in India: not always through hacking, but through pressure, trickery, fake authority, and rushed actions. Immediate action matters because cyber fraud response systems are designed to work fastest when a victim reports the transaction quickly enough for authorities, banks, and payment intermediaries to try to trace or freeze the funds before they are moved out.[pib.gov]

Featured Snippet Answer

Can UPI fraud money be recovered?

Yes, UPI fraud money can sometimes be recovered, especially if the fraud is reported within minutes or at least the same day and the money is still available in the beneficiary chain. Recovery is not guaranteed, but quick reporting through 1930, the cybercrime portal, your bank, and the UPI app significantly improves the chances of fund freezing, tracing, investigation, and possible refund.[paytm]

What Is UPI Fraud?

UPI fraud is any deceptive or unauthorized use of the Unified Payments Interface to move money out of a user’s account without genuine informed consent. In practice, this may involve fake collect requests, QR-code scams, phishing links, remote access apps, screen-sharing traps, SIM swaps, impersonation calls, or social engineering where the victim is manipulated into approving the transaction themselves.[phonepe]

UPI itself is only the payment rail. A UPI fraud may involve your bank, your UPI app, a payment service provider bank, and the destination bank account, which is why complaint handling often passes through multiple entities before a resolution is reached.[paytm]

UPI fraud types at a glance

| Fraud Type | Description | Recovery Possibility |

| Unauthorized debit after scam call | Victim is tricked into approving a payment or collect request | Moderate to high if reported immediately; lower if delayed [i4c.mha.gov] |

| QR code scam | Victim scans a code believing money will be received, but actually authorizes payment | Moderate if funds can still be frozen [paytm] |

| Fake customer care fraud | Fraudster pretends to be support staff and gets victim to disclose details or approve a transaction | Moderate, depends on speed and evidence [paytm] |

| Remote access or screen-sharing scam | Fraudster watches screen or controls device to induce or facilitate payment | Moderate to low, depending on how quickly reported [phonepe] |

| SIM swap or account takeover | Fraudster gains control over mobile-linked services and may facilitate unauthorized transactions | Case-specific; may improve if bank-side negligence or fast reporting is shown [anevagi] |

| Marketplace scam | Victim pays for goods or receives fake buyer/seller requests through UPI | Low to moderate unless reported very quickly [i4c.mha.gov] |

First 30 Minutes After UPI Fraud

This is the most important part of the entire UPI Fraud recovery process. The first 30 minutes can decide whether your money is still traceable inside the system or already layered across accounts and withdrawn.[i4c.mha.gov]

Immediate action plan

| Time | Action |

| Within 5 Minutes | Call 1930 and report the UPI fraud for recovery asap [i4c.mha.gov] |

| Within 10 Minutes | File a complaint on the National Cyber Crime Reporting Portal [i4c.mha.gov] |

| Within 15 Minutes | Notify your bank and ask for account and UPI risk controls if needed [hdfc.bank] |

| Within 20 Minutes | Raise a dispute in the UPI app used for the transaction [support.google] |

| Within 30 Minutes | Save all evidence: UTR, screenshots, call logs, messages, IDs, complaint numbers [cybercrime.gov] |

1) Within 5 minutes: Call 1930

The government’s financial cyber fraud response system allows victims to report digital payment fraud through 1930, the national helpline for immediate reporting of financial cyber frauds. The reporting system is specifically intended for quick reporting of losses involving digital banking, cards, wallets, payment intermediaries, and UPI.[pib.gov]

When you call, be ready with:

- Your name and mobile number.

- Bank or wallet name.

- 12-digit transaction ID or UTR.

- Date and amount of the fraudulent transaction.

- A short, clear description of what happened.[cybercrime.gov]

2) Within 10 minutes: Report online

File the same complaint on the National Cyber Crime Reporting Portal at cybercrime.gov.in. The portal asks for incident date and time, incident details, ID proof, and for financial fraud cases specifically, the bank or wallet name, 12-digit transaction ID or UTR, date, and amount.[cybercrime.gov]

Do not skip the online complaint just because you called 1930. The online record creates a complaint trail you may need later for banks, police follow-up, escalations, and ombudsman complaints.[cybercrime.gov]

3) Within 15 minutes: Inform your bank

Call your bank’s customer care, use the in-app support channel, and if necessary visit the branch. Ask them to log an unauthorized transaction complaint, note the service request number, and tell them the matter has also been reported through 1930 and the cybercrime portal.[hdfc.bank]

If you suspect account compromise beyond one payment, ask the bank about temporary controls such as blocking UPI, freezing risky channels, or changing credentials. That will not reverse the fraud automatically, but it may stop additional losses.[paytm]

4) Within 20 minutes: Raise dispute in the UPI app

Open the app used for the transaction and raise a complaint against the specific payment. Google Pay, PhonePe, Paytm, and other apps provide transaction-level issue reporting, and unresolved cases can move through app, bank, and NPCI-linked dispute paths.[support.google]

5) Within 30 minutes: Save evidence

Take screenshots of:

- Transaction page.

- UTR/reference number.

- Debit SMS.

- Bank statement entry.

- Scam chat, link, QR, or caller details.

- Your complaint reference numbers from 1930, cybercrime portal, bank, and app.[cybercrime.gov]

Speed matters because if funds are still in the recipient chain, timely complaints may help trigger tracing and freezing attempts. If the fraudster has already transferred or withdrawn the money, recovery becomes harder.[paytm]

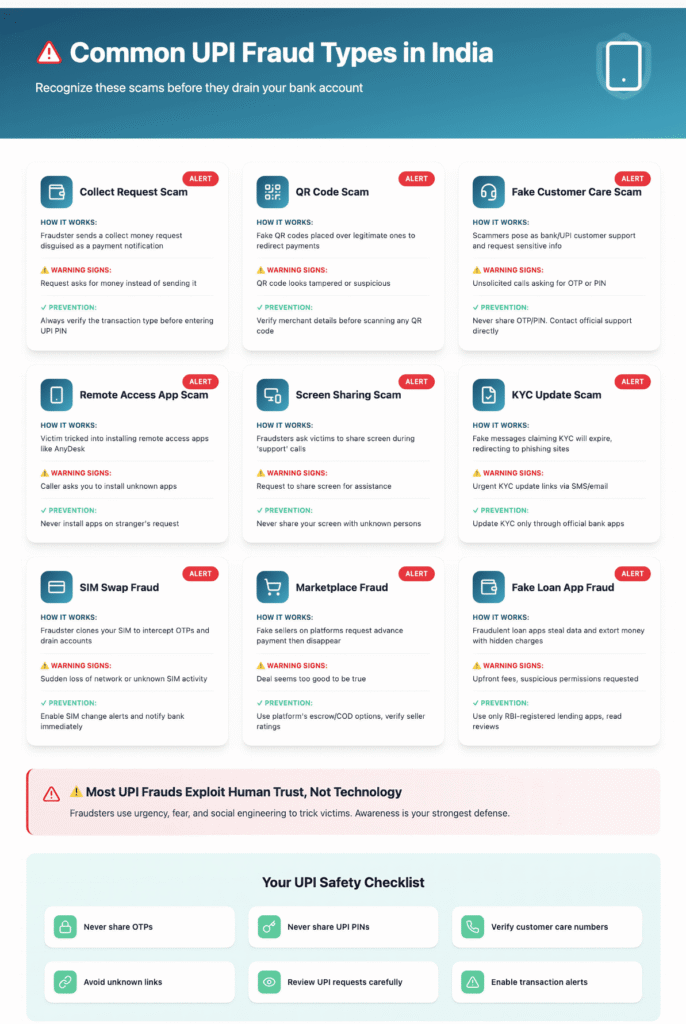

Common Types of UPI Frauds in India

Collect Request Fraud

In this scam, the fraudster sends a UPI “collect” request and tells the victim that approving it will receive money. In reality, approving a collect request authorizes a debit from the victim’s account.[payu]

Warning signs:

- “Approve to receive refund.”

- “Accept request to get payment.”

- Pressure to act fast.

Prevention:

- Read every UPI screen carefully.

- Remember: entering UPI PIN usually means money is going out, not coming in.

- Reject collect requests from unknown parties.

QR Code Scam

The scammer says they are sending you money, refunding you, or verifying your account and asks you to scan a QR code. Many victims believe scanning a QR code is only for receiving money, but in fraud setups it may lead to an outgoing payment flow.[paytm]

Warning signs:

- Stranger wants you to scan a code to “receive” funds.

- Seller/buyer claims QR scan is required for verification.

- Urgent refund or reward claim.

Prevention:

- Do not scan unknown QR codes for receiving money.

- Verify the flow shown on your app before entering your PIN.

- Confirm the payee name and purpose.

Fake Customer Care Scam

Fraudsters pose as customer support from a bank, wallet, shopping site, or app. They may ask you to install another app, share details, or follow steps that end in an unauthorized payment.[phonepe]

Warning signs:

- Random support number found through search or social media.

- Requests for OTP, PIN, screen-share access, or “verification payment.”

- Threats such as “account will be blocked.”

Prevention:

- Use only official support numbers from the app or bank website.

- Never share PINs or OTPs.

- Never follow support instructions from unofficial numbers.

Remote Access App Scam

The scammer persuades the victim to install a remote access app in the name of KYC, refund, service, or account help. Once installed, the fraudster can observe activity and manipulate the user into authorizing payments.[phonepe]

Warning signs:

- Request to install AnyDesk, TeamViewer, or similar tools.

- “We need device access to fix your account.”

- “Open your bank app while I guide you.”

Prevention:

- Never install remote access apps for banking support.

- Uninstall suspicious apps immediately.

- Review app permissions on your phone.

Screen Sharing Scam

This is similar to remote access fraud, but even simple screen-sharing can expose OTPs, balances, UPI IDs, and transaction flows. Some fraudsters do not need full device control if they can watch the screen and socially engineer the user.[phonepe]

Prevention: Never share your screen while using a banking or UPI app.

KYC Update Fraud

The scammer claims your KYC is expiring and your account or wallet will stop working unless you update immediately. The process usually leads to credential theft or unauthorized approval of a payment.[paytm]

Prevention: Do KYC updates only through the official app, branch, or verified bank channels.

SIM Swap Fraud

In SIM swap fraud, a criminal tries to take control of the mobile number linked to your bank and UPI. This can assist in account access, resets, or takeover attempts, especially when combined with other stolen information.[anevagi]

Prevention: Treat sudden SIM outage, no signal, or unexplained OTP activity as urgent warnings and contact your telecom operator and bank immediately.

Phishing Links

Victims receive links by SMS, WhatsApp, email, or social media asking them to claim rewards, unblock accounts, update KYC, or check refunds. These links often steal credentials or redirect users into scam workflows.[cybercrime.gov]

Prevention: Avoid clicking payment-related links from unknown or unverified sources.

Fake Loan App Fraud

The fraud may begin as a loan application but later turn into extortion, forced repayments, privacy abuse, or deceptive payment demands through UPI.[cybercrime.gov]

Prevention: Use only regulated lenders and verified apps from trusted publishers.

Marketplace Fraud

Common in OLX-style or social commerce deals, this scam can target both buyers and sellers. Fraudsters send fake buyer requests, demand token payments, or push collect requests disguised as sale proceeds.[paytm]

Prevention: Verify counterparties, avoid pressure payments, and never approve unexpected payment requests.

Can You Actually Recover Money Lost Through UPI Fraud?

Yes, sometimes—but not always. The honest answer is that recovery is possible, especially when the complaint is filed quickly enough for authorities and banks to act before the funds are moved, layered, or withdrawn.[i4c.mha.gov]

Recovery probability by reporting speed

| Situation | Recovery Probability |

| Reported within minutes | High compared with delayed reporting because tracing and freezing chances are better [i4c.mha.gov] |

| Reported same day | Moderate; action is still possible, but the fraudster may already have moved funds [i4c.mha.gov] |

| Reported after several days | Low; money may already be withdrawn or dispersed [i4c.mha.gov] |

Why timing changes outcomes

Recovery often depends on whether the beneficiary account still holds the funds or whether subsequent banks in the chain can freeze them. Once the money is cash-withdrawn, converted, or spread across mule accounts, the practical chances of getting it back fall sharply.[i4c.mha.gov]

Banks and payment entities may try to trace the transaction path, verify the recipient account, and process disputes, but they cannot guarantee reversal in every fraud case. UPI payments are generally not cancellable after authorization, which is why unauthorized transaction rules, complaint handling, and evidence become so important.[support.google]

Step-by-Step UPI Fraud Recovery Process

Below is the typical complaint and recovery journey many victims go through:

Victim detects fraud

↓

Calls 1930

↓

Cyber complaint registered

↓

Bank notified

↓

Beneficiary bank contacted

↓

Funds frozen (if possible)

↓

Investigation

↓

Refund decision

Stage-by-stage explanation

Victim detects fraud: The process starts the moment the victim notices an unauthorized debit, suspicious collect request approval, fake refund scam, or account compromise. Evidence should be preserved immediately.[cybercrime.gov]

Calls 1930: The helpline creates an urgent reporting path for financial cyber fraud cases, designed to support rapid intervention.[pib.gov]

Cyber complaint registered: The complaint may be logged through the helpline and/or portal, creating a formal case trail.[cybercrime.gov]

Bank notified: Your bank records the complaint, tags the transaction, and may start its own fraud workflow.[hdfc.bank]

Beneficiary bank contacted: In multi-party payment systems, complaint handling may involve the app, the PSP bank, and the beneficiary bank.[paytm]

Funds frozen if possible: If the money is still available in the destination chain, freezing attempts may occur. This is one reason immediate reporting matters so much.[paytm]

Investigation: The app, bank, and payment system participants review transaction data, logs, account details, and complaint evidence.[support.google]

Refund decision: Depending on facts, rules, evidence, and fund availability, the outcome may be full recovery, partial recovery, no recovery, or further escalation.[sansad]

How to Report UPI Fraud Through 1930 Cyber Helpline

1930 is India’s helpline for immediate reporting of financial cyber frauds. It replaced the earlier 155260 system and is linked to the financial cyber fraud reporting and management framework for quick action on digital payment frauds.[pib.gov]

How it works

When you call, the operator logs the fraud details and feeds them into the cyber financial fraud reporting system. The goal is fast intervention, especially in cases involving digital banking, payment intermediaries, cards, wallets, and UPI.[i4c.mha.gov]

What information you should keep ready

- Full name and contact number.

- Bank name or wallet/app name.

- UPI ID involved.

- 12-digit transaction ID or UTR.

- Transaction date and time.

- Amount lost.

- Short description of how the scam happened.

- Scammer mobile number, email, UPI ID, QR, or link if available.[cybercrime.gov]

What happens after reporting

You should receive or note a complaint reference that can help in follow-up. Reporting through 1930 does not replace reporting to your bank or the app, so all channels should be used in parallel for the best chance of action.[paytm]

1930 checklist

- Note exact transaction time.

- Keep UTR/reference number ready.

- Write down the fraud amount.

- Save screenshots first if possible.

- Call 1930 without waiting for the fraudster to “respond.”

- Record the complaint number carefully.[cybercrime.gov]

How to Report UPI Fraud on the National Cyber Crime Portal

The official portal is cybercrime.gov.in, and it is meant for online cybercrime reporting, including financial fraud complaints.[cybercrime.gov]

Step-by-step guide

- Visit the portal and choose the financial fraud complaint option.[cybercrime.gov]

- Log in or create the required citizen credentials if prompted.[cybercrime.gov]

- Enter the incident date and time.[cybercrime.gov]

- Describe the incident clearly in the complaint text.[cybercrime.gov]

- Upload ID proof in the permitted format.[cybercrime.gov]

- For financial fraud, enter the bank/wallet/merchant name, transaction ID or UTR, transaction date, and amount.[cybercrime.gov]

- Upload screenshots and supporting evidence.[cybercrime.gov]

- Submit the complaint and save the acknowledgement or complaint reference.[cybercrime.gov]

Required documents and details

The portal specifically asks complainants in financial fraud cases to keep the bank or wallet name, 12-digit transaction ID/UTR, transaction date, fraud amount, complainant ID proof, and relevant evidence ready.[cybercrime.gov]

Tracking complaint status

The cybercrime portal provides complaint tracking functionality, so keep the complaint number and any login credentials safe. Tracking helps if you later need to coordinate with police, bank teams, or escalation channels.[cybercrime.gov]

How to Raise UPI Fraud Complaints Through Popular Apps

App processes change over time, so users should verify the latest interface inside the app. Still, the complaint route usually begins with transaction history, selecting the disputed payment, and using “Help,” “Report issue,” or a similar dispute option.[payu]

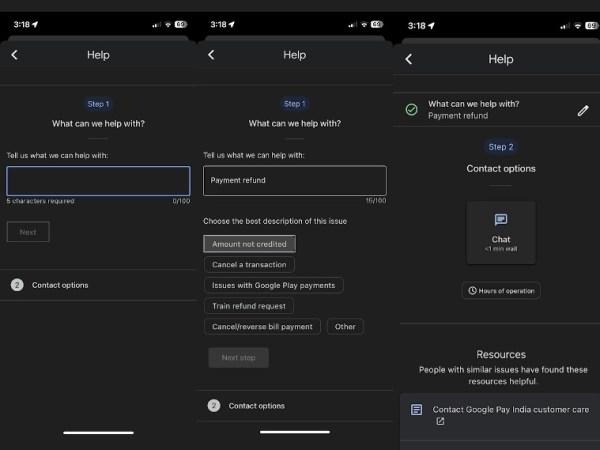

Google Pay

Google Pay’s help pages indicate that users can go to transaction history, choose the relevant transaction, and create a ticket through the issue flow. For unresolved UPI issues, Google Pay also points users toward contacting the bank and, if needed, escalating through NPCI’s dispute redressal mechanism.[support.google]

| Google Pay step | What to do |

| Find transaction | Open transaction history and select the payment [support.google] |

| Raise issue | Use “Having issues?” or the complaint flow shown in the app [support.google] |

| Add evidence | Upload bank statement or attachments if prompted [support.google] |

| Escalate | Contact your bank with the UPI reference ID; use NPCI route if unresolved [support.google] |

1. Find Transaction → Open Transaction History and Select Payment

This screenshot from a Google Pay Help page shows the transaction-history navigation and “Check transaction status” flow.

Source reference: Google Pay Help screenshot showing “Open Google Pay → All Transactions” flow.

Step 1: Open Google Pay and navigate to “All Transactions” to locate the disputed payment.

2. Raise Issue → Use “Having Issues?” / Complaint Flow

Step 2: Open the transaction and tap “Having issues?” or the relevant support option to raise a dispute.

3. Add Evidence → Upload Documents and Attachments

Google generally requests evidence during support interactions. Since exact in-app screenshots change frequently, use a supporting illustration rather than claiming a specific UI.

A better option is to create your own annotated screenshot showing:

- Transaction ID

- UPI Reference Number

- Bank Statement PDF

- SMS Alert

- Fraud Complaint Number

4. Escalate to Bank and NPCI

For this section, use a process infographic instead of a screenshot:

Google Pay Complaint

↓

Bank Customer Care

↓

Bank Nodal Officer

↓

NPCI UPI Dispute Process

↓

RBI Ombudsman (if needed)

PhonePe

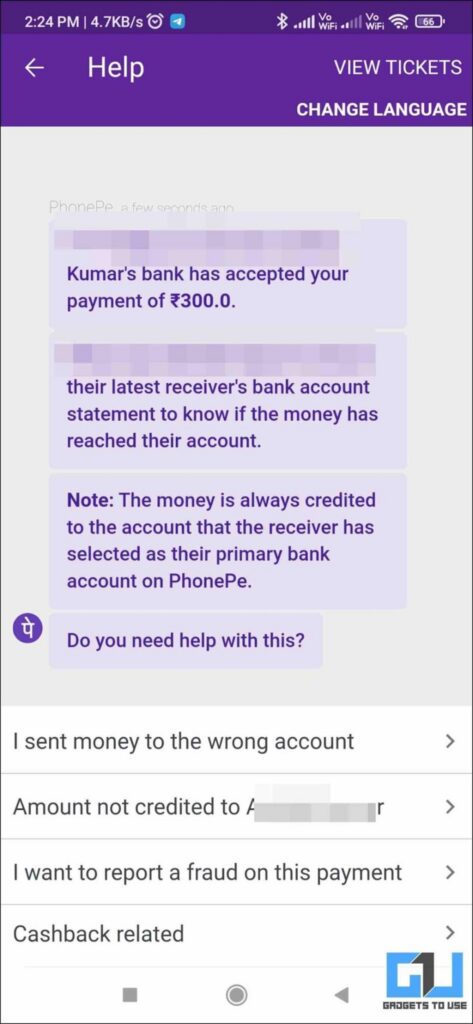

PhonePe says users can open the app, go to Help, choose the issue with the transaction, and submit a report. It also lists support channels including customer care numbers, a support webform, and a grievance portal for already raised tickets.[phonepe]

| PhonePe step | What to do |

| In-app complaint | Help section → transaction issue → report issue [phonepe] |

| Fraud category | Choose the option matching the scam, such as fraudster request or fraud call [phonepe] |

| Support channels | Call 080-68727374 or 022-68727374, or use the support webform [phonepe] |

| Escalation | Use the grievance portal for existing tickets [phonepe] |

1. In-App Complaint → Help Section → Transaction Issue → Report Issue

Step 1: Open PhonePe, go to the relevant transaction, and select the option to report an issue from the Help or Support section.

2. Fraud Category → Select the Appropriate Scam Type

Step 2: Choose the category that best matches the fraud, such as unauthorized payment, fraud call, collect request scam, or QR code fraud.

3. Support Channels → Contact PhonePe Support

Use a custom infographic instead of a screenshot.

PhonePe Customer Support

📞 080-68727374

📞 022-68727374

OR

Submit Complaint

via PhonePe Support Portal

Keep Ready:

✓ Transaction ID

✓ UPI Reference Number

✓ Screenshots

✓ Bank Statement

Step 3: If the in-app complaint does not resolve the issue, contact PhonePe customer support and provide all transaction details.

4. Escalation → Grievance Portal for Existing Tickets

Step 4: Escalate unresolved complaints through the grievance portal using your existing support ticket number.

Paytm

Paytm’s support material says fraudulent UPI transactions should be reported immediately through the UPI application, bank helpline, NPCI portal, and cybercrime reporting channels. It also advises contacting the bank to block the account or UPI services if necessary.[paytm]

| Paytm step | What to do |

| In-app complaint | Open support/help and raise a UPI or fraud complaint [paytm] |

| Parallel reporting | Inform bank and report on cybercrime portal or 1930 [paytm] |

| Escalation | NPCI dispute route if unresolved [paytm] |

BHIM

BHIM-related support guidance available through public help content suggests complaint flows usually begin from the transaction list or help section, followed by selecting the suspicious transaction and using a report issue option. Escalation may include BHIM support channels and broader NPCI-linked grievance routes.[community.finanjo]

Amazon Pay

Amazon Pay UPI users should follow the same general framework: raise the issue inside the app, contact the bank tied to the UPI transaction, report to 1930/cybercrime portal, and escalate through applicable dispute channels if unresolved. The exact interface can vary by app version, so users should rely on the current in-app help path and official support pages.[payu]

RBI Rules on Unauthorized Electronic Transactions

RBI’s customer protection framework on unauthorized electronic banking transactions is one of the most important rule sets for victims to understand. It lays out situations of zero liability, limited liability, and customer liability depending on who was at fault and how quickly the incident was reported.[anevagi]

Liability comparison

| Situation | Customer Liability |

| Fraud, negligence, or deficiency on the part of the bank | Zero liability for the customer [anevagi] |

| Third-party breach, neither bank nor customer at fault, and customer reports within 3 working days | Zero liability [anevagi] |

| Third-party breach reported in 4 to 7 working days | Limited liability, subject to RBI framework and account type caps/policy rules [anevagi] |

| Customer negligence, such as sharing payment credentials | Customer bears loss until the bank is informed; losses after reporting are to be borne by the bank [anevagi] |

| Reporting delay beyond 7 working days | Liability depends on the bank’s board-approved policy [anevagi] |

Important points readers should know

Under the RBI framework, where the bank is at fault or where a qualifying third-party breach is reported in time, the customer may have zero liability. The framework also states that on being notified, the bank must credit the amount involved in the unauthorized electronic transaction to the customer’s account within 10 working days through a shadow reversal in applicable cases.[sansad]

This is educational information, not legal advice. Whether a specific UPI fraud qualifies under these rules depends on facts such as customer actions, app approvals, credential sharing, and transaction circumstances.[anevagi]

What Banks Do Internally After a Fraud Complaint

Most users imagine that a complaint simply “goes to the bank,” but internally the process is usually more layered. Depending on the case, the bank may review transaction logs, customer complaint records, device and channel data, account history, and inter-bank message trails connected to the UPI transaction.[paytm]

If a UPI app is involved, the complaint may first touch the third-party app provider, then move to the PSP bank, and then involve the beneficiary bank if the case remains unresolved or requires deeper review. Public descriptions of NPCI-linked complaint handling indicate time windows for app-level review and escalation to participating banks.[paytm]

In practical terms, banks may also send fund-freezing or information requests where possible, verify whether the beneficiary account still holds the money, and decide whether the matter appears to be an unauthorized transaction, customer-authorized payment under deception, failed transaction, wrong transfer, or another dispute category. That classification can significantly affect how the case is handled and the user’s chances of refund.[support.google]

UPI Fraud Refund Timeline

Recovery timelines vary widely. Some complaints move quickly if the funds are still available, while others drag on because multiple institutions are involved or because the facts are disputed.[idfcfirst.bank]

Typical timeline

| Stage | Expected Timeline |

| Complaint filing | Immediate, as soon as user calls 1930 or files online/in-app [i4c.mha.gov] |

| Initial review | 24-72 hours is common for first-level acknowledgement or review movement, though exact timelines vary by entity [paytm] |

| Investigation | Around 7-30 days in many dispute situations, depending on complexity and inter-bank coordination [paytm] |

| Resolution | Can extend up to 90 days or more in some complaint frameworks and escalations [idfcfirst.bank] |

Why delays happen

Delays can happen when:

- The money has already moved through multiple accounts.

- More than one bank is involved.

- The customer’s version and transaction logs conflict.

- The complaint is incomplete or lacks evidence.

- The case needs escalation beyond first-line support.[idfcfirst.bank]

Documents and Evidence Required for Recovery

Evidence quality often affects both the speed and seriousness of the response. A victim who can produce a clean evidence trail usually has a better chance of getting the complaint understood correctly and escalated efficiently.[cybercrime.gov]

Evidence checklist

| Document / Proof | Why it matters |

| Transaction ID / UTR | Core identifier used to trace the payment [cybercrime.gov] |

| Screenshots of the transaction | Shows amount, time, payee, and status [cybercrime.gov] |

| Bank statement or passbook entry | Confirms debit from the account [support.google] |

| SMS or app alerts | Helps establish timing and sequence [cybercrime.gov] |

| Fraudster mobile number / UPI ID / QR / link | Supports tracing and case classification [cybercrime.gov] |

| Call recordings or chat screenshots | Useful to prove deception or impersonation [cybercrime.gov] |

| Complaint numbers from 1930 and cybercrime portal | Critical for follow-up and escalation [cybercrime.gov] |

| Bank complaint reference / SR number | Needed for bank escalation and ombudsman route [idfcfirst.bank] |

| Identity proof | Required on the cybercrime portal [cybercrime.gov] |

What If Your Bank Rejects the Complaint?

A rejection is not always the end of the road. If your bank refuses the complaint, gives a partial response, or does not respond within a reasonable period, the matter can usually be escalated through the bank’s internal grievance mechanism and then to the RBI ombudsman framework where applicable.[financialservices.gov]

Escalation path

- Re-raise the complaint with the bank’s grievance or nodal officer, attaching all earlier complaint references and evidence.[idfcfirst.bank]

- If the bank does not respond within 30 days, or the response is unsatisfactory, file a complaint under the RBI Integrated Ombudsman Scheme through cms.rbi.org.in or the channels listed by RBI-linked support material.[support.google]

- Where needed, continue coordination with cybercrime authorities and consider independent legal advice for serious losses or disputed negligence issues.[financialservices.gov]

This is educational guidance, not legal advice. For complex disputes, especially involving large amounts, senior citizens, business accounts, or contested negligence, a qualified legal professional may help interpret documents and liability positions.

Real-Life UPI Fraud Recovery Scenarios

These are educational examples based on common complaint patterns, not records of specific identified individuals.

Case Study 1: Successful recovery

A user approved a fake collect request for ₹18,000 after believing it was a refund. Within 10 minutes, the user called 1930, filed the cybercrime complaint, alerted the bank, and raised a dispute in the app, giving authorities a chance to act while the funds were still in the destination chain. This type of fast, multi-channel reporting offers the strongest recovery chance because tracing and freezing efforts can begin quickly.[pib.gov]

Lesson: Speed is the single biggest factor working in the victim’s favor.

Case Study 2: Partial recovery

A small business owner lost ₹42,000 in a fake customer care scam but reported the issue only later the same evening. By then, part of the money had already been moved, though one linked amount remained traceable. In such cases, partial recovery can occur if only some funds remain available or if evidence supports only a limited reversal path.[paytm]

Lesson: Same-day reporting is still useful, but delay can reduce recovery.

Case Study 3: Recovery denied

A victim shared credentials and reported the fraud after several days, by which time the funds had been withdrawn. Under RBI’s framework, customer negligence and delayed reporting can affect liability, and in practice delayed cases become much harder to recover because the money may no longer be traceable in the system.[linkedin]

Lesson: Do not wait for the scammer to “return” the money or for the issue to fix itself.

How to Protect Yourself from Future UPI Frauds

- Never approve collect requests blindly. Many scams rely on victims misunderstanding approval prompts.[payu]

- Never share OTPs, UPI PINs, or other payment credentials. Customer negligence can affect liability outcomes.[linkedin]

- Verify UPI IDs and payee names before every payment.[support.google]

- Avoid scanning unknown QR codes, especially to “receive” money.[paytm]

- Never install screen-sharing or remote access apps for banking help.[phonepe]

- Ignore suspicious links about KYC, refunds, rewards, or account blocking.[cybercrime.gov]

- Enable transaction alerts and review them immediately. Fast detection supports faster reporting.[i4c.mha.gov]

- Use app locks and device security.[cybercrime.gov]

- Keep banking and UPI apps updated from official app stores.[cybercrime.gov]

- Monitor account activity regularly, especially if you are a senior citizen, business owner, or first-time digital payment user.[i4c.mha.gov]

Most Common Myths About UPI Fraud Recovery

| Myth | Reality |

| “UPI fraud money can never be recovered.” | Recovery is possible in some cases, especially with immediate reporting, but it is not guaranteed. [i4c.mha.gov] |

| “If I approved it once, nothing can be done.” | Even customer-authorized scam payments should still be reported immediately through all channels. [paytm] |

| “Only the bank can help.” | You should also use 1930, the cybercrime portal, the app complaint flow, and escalation channels. [i4c.mha.gov] |

| “1930 is only for advice.” | It is a helpline for immediate reporting of financial cyber frauds. [i4c.mha.gov] |

| “I should wait to see if the scammer refunds me.” | Delay reduces the chance of tracing or freezing funds. [i4c.mha.gov] |

| “UPI payments can simply be cancelled after completion.” | Completed UPI transactions are generally not cancellable just because you changed your mind. [support.google] |

| “NPCI directly refunds every fraud case.” | NPCI is part of the dispute ecosystem, but refunds depend on facts, rules, and fund availability. [paytm] |

| “If the bank rejects me once, the case is over.” | You may still escalate through the bank grievance route and the RBI ombudsman process. [idfcfirst.bank] |

| “Only hacked accounts count as unauthorized transactions.” | Fraud can also happen through deception, impersonation, collect requests, phishing, or remote access scams. [paytm] |

| “Screenshots are enough; I do not need complaint numbers.” | Complaint references from the bank, portal, and helpline are crucial for follow-up. [cybercrime.gov] |

Frequently Asked Questions

1) Can UPI fraud money be recovered?

Sometimes, yes. Recovery is most likely when the fraud is reported quickly and the funds can still be traced or frozen before being withdrawn or moved onward.[pib.gov]

2) What is the cyber fraud helpline number?

The helpline for immediate reporting of financial cyber frauds in India is 1930.[pib.gov]

3) How long does UPI refund take?

There is no single guaranteed timeline. Complaint acknowledgement can be immediate, early review may begin in days, investigation may take weeks, and escalated resolution can stretch much longer depending on the case.[idfcfirst.bank]

4) Can police recover UPI fraud money?

Cybercrime authorities can support tracing, investigation, and coordination, especially when the complaint is filed quickly through the official system. Actual recovery still depends on whether the money remains traceable and legally recoverable.[i4c.mha.gov]

5) What proof is required?

The most important proof includes the UTR or transaction ID, screenshots, bank statement, SMS alerts, complaint references, and any scammer contact or communication details.[cybercrime.gov]

6) Can banks reverse UPI transactions?

Banks may be able to process dispute and recovery actions in some cases, but completed UPI transactions are not simply “cancelled” after authorization. Outcomes depend on the facts, the complaint category, liability rules, and fund availability.[support.google]

7) What if the fraudster has already withdrawn the money?

Recovery becomes much harder once funds are withdrawn or dispersed. That does not mean you should stop reporting, but expectations should be realistic.[paytm]

8) Does NPCI provide refunds?

NPCI is part of the UPI dispute and complaint framework, but it is not a blanket refund provider for every scam. Cases may pass through app-level review, PSP banks, and dispute mechanisms before resolution.[paytm]

9) What if my bank refuses to help?

Escalate to the bank’s grievance or nodal officer, and if the bank does not respond within 30 days or gives an unsatisfactory response, consider the RBI Integrated Ombudsman route where applicable.[support.google]

10) Can I approach RBI?

Yes, after first raising the matter with the bank and waiting through the required complaint process. RBI’s ombudsman complaint channels are available for eligible unresolved grievances.[financialservices.gov]

11) Can I get compensation?

That depends on the facts, the applicable banking rules, and whether there was bank deficiency, unauthorized transaction protection, or another legally recognized basis. No compensation should be assumed automatically.[sansad]

12) Is UPI fraud covered by insurance?

Sometimes certain personal cyber insurance or bank-linked protection products may offer limited coverage, but this is product-specific and not a universal UPI rule. Users must check policy wording carefully. Official recovery systems remain the first response route.[financialservices.gov]

13) Can senior citizens recover money lost in fraud?

Yes, senior citizens can and should use the same reporting channels immediately. In practice, quick reporting, family support, clear evidence, and branch assistance can be especially helpful for elderly users.[i4c.mha.gov]

14) What happens after filing a cyber complaint?

The complaint enters the cyber fraud reporting system, and depending on the case it may trigger bank and payment participant review, tracing efforts, and further investigation. Additional follow-up may still be needed with the bank and app.[paytm]

15) How do I track my complaint?

Use the acknowledgement or complaint reference from the cybercrime portal’s tracking system, along with your bank complaint number and app ticket ID. These references are essential for follow-up.[cybercrime.gov]

16) Should I also file a complaint in the UPI app?

Yes. App-level complaint flows form part of the dispute chain and should be used alongside bank and cybercrime reporting.[support.google]

17) Should I visit the bank branch?

If the amount is large, your account may be compromised, or you are not getting clear help remotely, a branch visit can be useful in addition to phone and online complaints. Bank reference numbers and written acknowledgement are valuable.[hdfc.bank]

Key takeaways

- Act immediately: Call 1930, file on cybercrime.gov.in, inform your bank, and raise an in-app dispute without delay.[paytm]

- Keep evidence ready: UTR, screenshots, statements, alerts, scammer details, and complaint numbers matter.[cybercrime.gov]

- Do not expect guarantees: Some victims recover all, some recover part, and some do not recover anything. Timing, facts, and fund availability matter.[support.google]

- Know your rights: RBI’s unauthorized electronic transaction framework can help in qualifying cases, especially where bank deficiency or timely reported third-party breach is involved.[anevagi]

- Protect yourself going forward: Never share OTPs or PINs, never approve collect requests blindly, and never install remote-access tools for payment support.[anevagi]

If you have just been scammed, stop reading and report the fraud right now. Early reporting gives the best chance of tracing the transaction, freezing funds where possible, and improving the odds of recovery.[paytm]