If you have lost money to an online scam, UPI fraud, fake investment scheme, or any other cyber fraud, the National Cyber Crime Reporting Portal is your first and most important stop. This guide walks you through everything — what NCRP is, how to file a complaint, what happens after you file, and whether you can realistically recover your money.

NCRP (National Cyber Crime Reporting Portal) is India’s official government platform at cybercrime.gov.in for reporting all types of cybercrime. Any Indian citizen who has suffered online fraud, UPI scam, investment fraud, or digital crime should use it. Report as fast as possible — ideally within the first hour. Early reporting dramatically improves the chances of freezing fraudulent accounts before money is withdrawn. Recovery is possible but not guaranteed.

Table of Contents

Quick Summary Table

| Question | Answer |

| What is NCRP? | National Cyber Crime Reporting Portal — India’s official cybercrime complaint platform |

| Official Website | cybercrime.gov.in |

| Helpline Number | 1930 |

| Can Money Be Recovered? | Sometimes — depends on speed of reporting and investigation |

| Complaint Filing Cost | Free |

| Complaint Tracking Available? | Yes — via acknowledgment number on the portal |

| Best Time to Report Fraud | Immediately — within the first hour if possible |

| Investigation Authority | State Cyber Crime Cells coordinated by I4C (Indian Cyber Crime Coordination Centre) |

What Is NCRP?

NCRP stands for National Cyber Crime Reporting Portal. It is an initiative of the Ministry of Home Affairs, Government of India, operated through the Indian Cyber Crime Coordination Centre (I4C).

The portal was launched to give every Indian citizen a single, centralized platform to report cybercrime — from anywhere in the country, at any time, without needing to physically visit a police station.

Before NCRP existed, cybercrime victims had to approach their local police station. Most stations lacked the technical expertise to handle digital fraud. Cases fell through the cracks. Perpetrators — often operating from other states or countries — went unpursued.

NCRP changed this by:

- Creating a national database of cybercrime complaints

- Automatically routing complaints to the correct state cyber cell

- Enabling coordination between banks and law enforcement for rapid fund freezing

- Allowing victims to track complaint progress online

- Providing the 1930 financial fraud helpline for urgent cases

The portal handles all categories of cybercrime — from ₹500 UPI fraud to multi-crore cryptocurrency investment scams.

Types of Cybercrimes You Can Report Through NCRP

| Crime Category | Examples | Key Evidence Needed |

| UPI Fraud | Fake payment requests, QR code scams | Transaction ID, UPI reference, screenshots |

| Internet Banking Fraud | Unauthorized transfers, phishing | Transaction reference, bank statement |

| Credit/Debit Card Fraud | Unauthorized card transactions | Card statement, transaction ID |

| Investment Scams | Fake trading platforms, fixed return schemes | Platform URL, payment receipts, chat records |

| Cryptocurrency Fraud | Fake exchanges, pig butchering, rug pulls | Wallet addresses, exchange screenshots, TXIDs |

| Job Scams | Fake employment offers, advance fee fraud | Job offer letter, payment receipts, chat records |

| Lottery/Prize Scams | Winning notices requiring advance payment | Communication records, payment proof |

| Impersonation Fraud | Fake bank officials, CBI/police impersonation | Call records, transaction proof |

| Social Media Fraud | Fake profiles, account hacking, blackmail | Screenshots, profile URLs, messages |

| Matrimonial Fraud | Fake profiles on matrimony sites | Profile screenshots, communication records |

| Sextortion | Threats using intimate images | Communication records, screenshots |

| Identity Theft | PAN misuse, Aadhaar misuse | Identity documents, fraud transaction proof |

| Child Safety Issues | CSAM, online grooming | Evidence handled sensitively by authorities |

| OTP Fraud | Fraudsters obtaining OTPs to access accounts | Call records, bank transaction details |

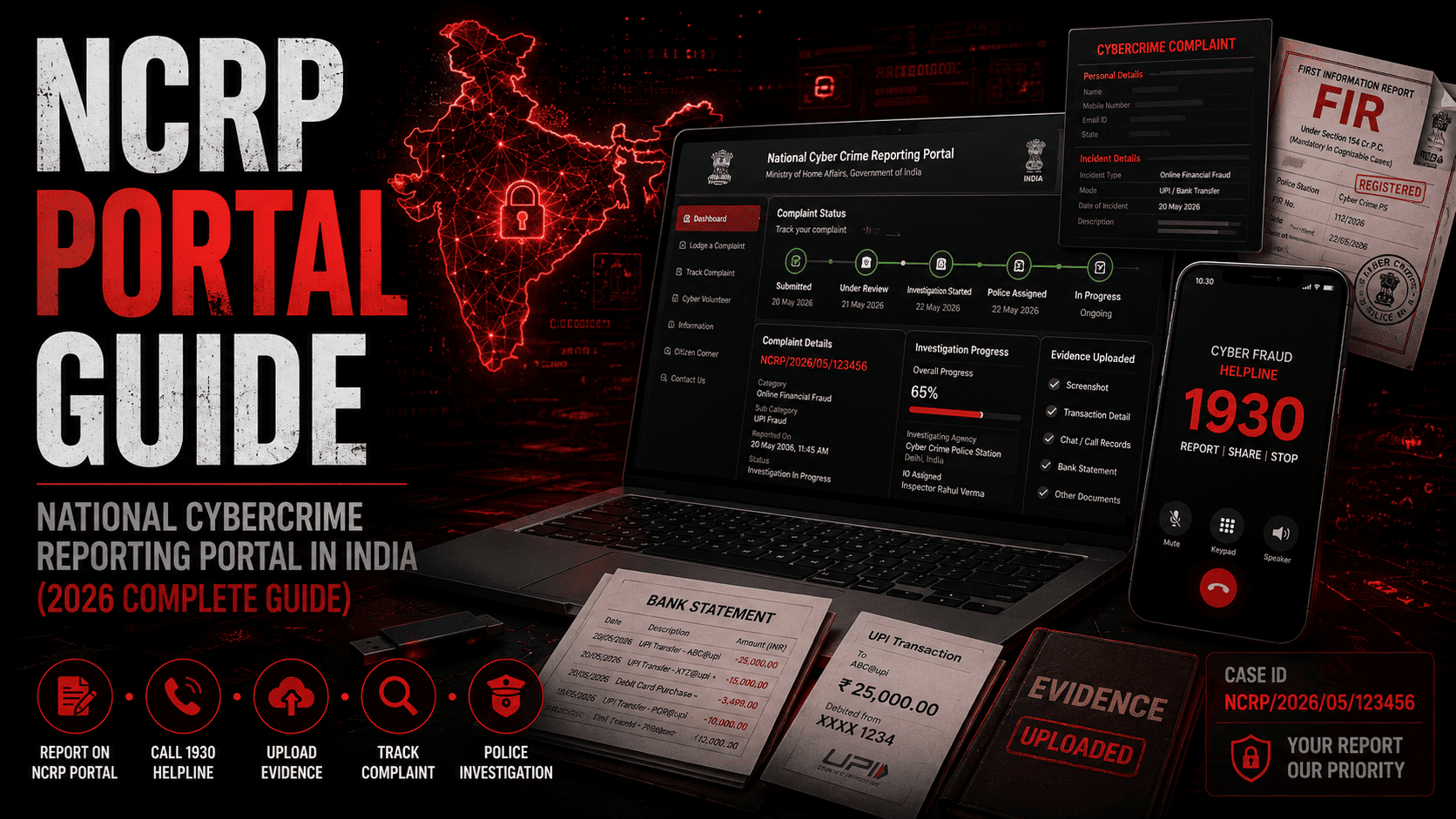

Cybercrime Helpline 1930 Explained

1930 is the single most important number every Indian should save in their phone.

This dedicated financial cybercrime helpline operates specifically to help fraud victims report and freeze fraudulent transactions in real time. When you call 1930 immediately after a fraud, the helpline operator can coordinate with your bank and the fraudster’s bank to freeze the destination account before the money is withdrawn.

This is the golden hour of cybercrime reporting. Just as heart attack treatment is most effective in the first hour, financial fraud recovery is most effective in the first 60 minutes.

What to have ready before calling 1930:

- Your bank account number and registered mobile number

- The exact amount lost and the time of the transaction

- Transaction ID, UTR number, or UPI reference number

- The account number or UPI ID the money was sent to

- Name of your bank and the fraudster’s bank (if visible)

- Brief description of how the fraud happened

When to call 1930:

Call 1930 before filing on the portal if the fraud just happened. The helpline triggers immediate banking coordination. The portal complaint can follow. Every minute matters for fund freezing.

How to File a Complaint on NCRP: Step-by-Step

Step 1: Visit the official portal Go to cybercrime.gov.in — only this URL. Beware of fake lookalike sites. The government never charges any fee to file a complaint.

Step 2: Register on the portal Click “File a Complaint.” Register with your mobile number. An OTP will be sent for verification. Create a login.

Step 3: Select your complaint category Choose between “Report Financial Fraud” (for money-related crimes) or “Report Other Cyber Crime” (for social media fraud, sextortion, identity theft, etc.). Financial fraud gets priority routing for bank coordination.

Step 4: Fill in incident details Enter the date and time of the fraud, the amount lost, the transaction details, the fraudster’s contact information (phone number, UPI ID, website URL, wallet address), and a clear description of what happened. Be specific and factual.

Step 5: Upload supporting evidence Attach screenshots, bank statements, transaction confirmations, chat records, and any other relevant files. The more evidence you upload, the stronger your complaint.

Step 6: Enter your personal details Provide your name, address, Aadhaar number, PAN, email, and mobile number. These are kept confidential and used for investigation purposes.

Step 7: Submit the complaint Review all information carefully before submitting. Once submitted, you cannot edit the complaint, but you can add information later.

Step 8: Save your acknowledgment number After submission, you receive an acknowledgment number. Save this immediately — it is your complaint reference for all future tracking and follow-up.

Documents Required for NCRP Complaint

| Document | Why It Helps |

| Aadhaar Card | Identity verification |

| PAN Card | Financial identity, KYC linkage |

| Bank Statement | Shows fraudulent transaction clearly |

| Transaction ID / UTR Number | Critical for bank coordination and fund tracing |

| UPI Reference Number | Essential for UPI fraud cases |

| Screenshots of fraud | Direct visual evidence |

| Chat/WhatsApp records | Proves fraudster communication |

| Email records | Documents phishing or scam communication |

| Fraudster’s phone number | Enables tracing |

| Platform URL | For investment or fake exchange scams |

| Crypto wallet addresses | For cryptocurrency fraud cases |

| Transaction Hash (TXID) | For blockchain tracing in crypto cases |

What Happens After Filing a Complaint?

This is what most victims want to know — and it is important to have realistic expectations.

| Stage | What Happens | Typical Timeline |

| Complaint Submission | Complaint logged, acknowledgment number generated | Immediate |

| Initial Review | Portal team verifies complaint details | 24–72 hours |

| Routing | Complaint assigned to relevant State Cyber Cell | 2–7 days |

| Banking Coordination | Cyber cell contacts bank to flag or freeze accounts | Varies; faster if reported immediately |

| Investigation Begins | IO assigned; evidence reviewed | 1–4 weeks |

| Suspect Identification | Transaction tracing, KYC data request from exchange/bank | Weeks to months |

| Legal Action | FIR filed, arrest if suspect identified | Months |

| Fund Recovery | Frozen funds released to victim via court process | Months to years |

What actually happens in the first 24 hours is the most critical. If you called 1930 first, bank coordination may have already started. If not, the cyber cell will initiate it as soon as the complaint is verified and routed.

Honest reality: Not every complaint results in an FIR. Not every FIR results in an arrest. Not every arrest results in recovery. But filing the complaint is essential — it creates a legal record, contributes to intelligence databases, and is a prerequisite for any bank-level or court-level recovery process.

How to Track Your NCRP Complaint Status

- Visit cybercrime.gov.in

- Click “Report & Track” then “Track Your Complaint”

- Enter your acknowledgment number and registered mobile number

- Enter the OTP sent to your mobile

- View current complaint status

Common Status Messages and Their Meanings

| Status | What It Means |

| Complaint Submitted | Successfully received; under initial review |

| Under Process | Being reviewed or routed to state cyber cell |

| Assigned | Forwarded to relevant state authority |

| Under Investigation | Actively being investigated by cyber cell |

| Additional Information Required | Authorities need more details from you — respond immediately |

| Closed | Investigation concluded; check for follow-up communication |

| Rejected | Complaint not accepted; reason provided |

If status shows “Additional Information Required,” respond within the stated deadline. Failure to respond can result in your complaint being closed without action.

Can You Recover Money Through NCRP?

This requires an honest answer. Recovery is possible — it is not guaranteed.

| Factor | Impact on Recovery |

| Reported within 1 hour | Very High — fund freeze before withdrawal possible |

| Reported within 24 hours | High — some freeze chances remain |

| Reported within 1 week | Moderate — funds may still be in banking system |

| Reported after 1 month | Low — funds likely moved or withdrawn |

| Fraudster used KYC-verified account | Higher — identity traceable |

| Fraudster used mule accounts | Lower — chain complicates tracing |

| Fraud within India | Higher — jurisdiction straightforward |

| Cross-border fraud | Lower — international cooperation required |

| Crypto fraud through mixer | Very Low — trace becomes extremely difficult |

| Large organized scheme | Lower for individuals; collective action helps |

When recovery is most likely: You called 1930 within the first hour, the money was still in the banking system, and the receiving account was KYC-verified at a regulated Indian bank.

When recovery is very difficult: The fraud happened weeks ago, funds were moved through multiple accounts, converted to crypto, or sent overseas.

Common Mistakes Victims Make

- Waiting before reporting. Every hour reduces recovery chances.

- Not calling 1930 first. The helpline triggers bank freezing — file portal complaint second.

- Deleting chat history with fraudster. This is key evidence. Preserve everything.

- Not saving the transaction ID. Without this, banking coordination is severely limited.

- Sending more money hoping to recover the first loss. A classic secondary scam trap.

- Telling the fraudster you are reporting them. They immediately move funds.

- Using screenshots that cut off important information. Capture full screen with all details visible.

- Filing complaint with incorrect transaction details. Errors slow investigation significantly.

- Not responding to “Additional Information Required” status. Cases close without your input.

- Trusting paid “NCRP complaint filing services.” NCRP is free. Anyone charging a fee is a scammer.

- Filing only on NCRP and not registering FIR. Both are needed for complete legal coverage.

- Assuming the complaint is enough. You must follow up actively.

- Not preserving bank statements. Download and save them immediately.

- Forgetting to note the fraudster’s phone number or UPI ID. Critical tracing information.

- Sharing your NCRP login or acknowledgment number with strangers. Keep this private.

- Believing scammers who claim to be “NCRP officers” calling to help. NCRP does not make unsolicited calls.

- Filing the complaint from the wrong category. Financial fraud must be filed under financial fraud for bank coordination.

- Providing vague descriptions. Be specific: exact amounts, exact times, exact sequence of events.

- Not following up with state cyber cell directly. Portal is step one; direct engagement accelerates results.

- Engaging fake recovery services after filing NCRP complaint. A very common secondary victimization.

Real-Life Scenarios

Case Study 1: UPI Scam

Kavitha from Chennai received a call from someone claiming to be from her bank. The caller said her account would be blocked unless she verified her UPI PIN. She shared the PIN. Within minutes, ₹42,000 was debited. She called 1930 within 20 minutes. The helpline coordinated with her bank and the destination bank. The receiving account was flagged. ₹38,000 was frozen before withdrawal. She filed on NCRP the same evening. Within 6 weeks, the frozen amount was returned through bank reversal coordination.

Read our blog on – “UPI Fraud Recovery In 2026”

Lesson: Calling 1930 immediately and before touching anything else saved nearly her entire loss.

Case Study 2: Investment Fraud

Ramesh from Pune invested ₹3.5 lakh in a fake trading platform over three months, believing his account showed ₹9 lakh in profits. When he tried to withdraw, the platform asked for a 20% “tax fee.” He then realized the scam. He reported to NCRP immediately with all transaction records, platform URLs, and chat history. The state cyber cell traced part of the funds to a domestic bank account and filed an FIR. One suspect was arrested. Partial recovery of ₹80,000 was facilitated.

Lesson: Comprehensive documentation across three months of transactions made the investigation significantly easier.

Case Study 3: Crypto Scam

Anita from Bengaluru lost ₹6 lakh to a pig butchering scam. She deleted the Telegram conversation with the fraudster out of embarrassment before reporting. When she filed on NCRP two weeks later, the blockchain trail showed funds had been moved through a mixer. Despite investigation efforts, recovery was not possible.

Lesson: Never delete communications. Report immediately. Delayed reporting in crypto scams is almost always fatal to recovery chances.

Case Study 4: Job Scam

Suresh, a recent graduate from Lucknow, paid ₹25,000 as a “training fee” to a fake company that promised remote employment. The company asked for additional payments after the first one. He stopped, searched the company name, found complaints online, and filed on NCRP the same day with all payment receipts and offer letters. Police identified the operator in another state. FIR was filed. Criminal proceedings began.

Lesson: Acting at the first suspicious sign — rather than continuing payments — limited the total loss and enabled investigation.

Case Study 5: Social Media Fraud

Priya from Delhi had her Instagram account hacked. The hacker messaged her followers claiming she was in an emergency and needed urgent money transfers. Several followers sent money. Priya filed complaints both for herself and on behalf of affected followers on NCRP. She also reported the fake account to Instagram. The cyber cell traced the account access to an IP address. Combined digital and law enforcement action led to identification of the suspect.

Lesson: Social media fraud affects not just the victim but their entire network. Report immediately and warn your contacts.

What To Do If NCRP Complaint Shows No Progress

If weeks have passed with no meaningful update, here is your escalation path:

- Follow up on the portal — check if “Additional Information Required” status is showing and respond.

- Contact State Cyber Cell directly — find your state cyber crime department’s contact details online and submit a written follow-up with your acknowledgment number.

- Visit your nearest police station — request registration of a formal FIR referencing your NCRP complaint number.

- Write to the SP (Cyber Crime) — a written complaint to the Superintendent of Police (Cyber) in your district often accelerates stalled cases.

- Approach a lawyer — for significant amounts, a lawyer can file representations to senior police officers or approach the Magistrate under BNSS provisions.

- High Court Writ — in cases of complete inaction over extended periods, a Writ Petition is available as a last resort.

30 Ways to Avoid Cyber Fraud

- Never share OTPs with anyone — no bank, no government officer, no one ever legitimately asks for them.

- Save 1930 in your contacts right now, before you ever need it.

- Verify any payment request by calling back on the official number — not the number the caller gives you.

- Never scan a QR code to receive money — QR codes are only for sending, not receiving.

- Check website URLs character by character before entering banking credentials.

- Use only apps downloaded from official app stores — never APKs sent via WhatsApp.

- Enable transaction limits on your UPI and banking apps.

- Never invest in schemes promising fixed daily or weekly returns.

- Verify any trading platform’s registration with SEBI before investing.

- Never pay a fee to receive a prize, lottery, or inheritance — it is always a scam.

- Do not click links in SMS messages claiming to be from banks or government agencies.

- Use unique, strong passwords for every financial account.

- Enable two-factor authentication on all email and social media accounts.

- Never allow anyone remote access to your phone or computer to help “fix” a problem.

- Verify job offers independently before paying any fee — legitimate employers never charge candidates.

- Never send money to romantic interests met online before meeting in person.

- Use only FIU-IND registered crypto exchanges — never unregulated platforms.

- For P2P crypto trades, use only platform escrow — never off-platform transfers.

- Call your bank immediately if you notice any transaction you did not authorize.

- Regularly check your credit report for unauthorized accounts or loans in your name.

- Keep your Aadhaar, PAN, and banking details off social media entirely.

- Be suspicious of any WhatsApp or Telegram group promising investment profits.

- Never respond to “your account will be blocked” urgency calls — call your bank directly.

- Verify the identity of anyone claiming to be police, CBI, or government official digitally.

- Do not use public Wi-Fi for any banking or financial transaction.

- Keep your mobile’s SIM registered in your name and report loss immediately to prevent SIM swap.

- Regularly review app permissions — revoke access to apps you no longer use.

- Educate elderly family members about common scam patterns regularly.

- Bookmark cybercrime.gov.in now so you always have the right URL.

- Trust your instincts — if something feels wrong, stop, verify independently, then proceed.

Expert Opinion: Why Early Reporting Through NCRP Matters

The concept of the “golden hour” in cybercrime is not a metaphor — it is operationally real.

India’s financial fraud response system is built around speed. When a victim calls 1930, the helpline has direct coordination channels with major Indian banks. In well-documented cases reported within the first hour, account freezes have been executed within minutes of the call.

The I4C has published data showing that complaints filed within 24 hours have significantly higher fund recovery rates than those filed later. After 72 hours, recovery rates drop substantially. After one week, most fraudsters have moved funds multiple times, making banking-layer recovery nearly impossible.

The digital payment ecosystem has made fraud faster than ever — UPI transactions are instant, irreversible at the user level, and cross bank boundaries seamlessly. The same infrastructure that makes payments convenient makes fraud movement fast.

Emerging threats in 2026 include AI-generated voice cloning (fraudsters mimicking family members’ voices to request emergency transfers), deepfake video calls from fake bank officials, and sophisticated crypto-layering that uses DeFi protocols to obscure fund trails.

In this environment, public awareness and immediate reporting are the most powerful tools available to ordinary citizens. NCRP and 1930 exist precisely for this purpose — use them the moment fraud happens.

Frequently Asked Questions

Q1. Is NCRP genuine and government-operated? Yes. The National Cyber Crime Reporting Portal at cybercrime.gov.in is a legitimate initiative of the Ministry of Home Affairs, Government of India. It is operated by I4C (Indian Cyber Crime Coordination Centre). Filing a complaint is completely free. Any website or person claiming to offer paid NCRP complaint filing or follow-up services is a scammer attempting to exploit fraud victims a second time.

Q2. How do I track my NCRP complaint? Visit cybercrime.gov.in, click “Report & Track,” then “Track Your Complaint.” Enter your acknowledgment number and registered mobile number, verify the OTP, and your complaint status will be displayed. Common statuses include Submitted, Under Process, Assigned, Under Investigation, Additional Information Required, and Closed. Check regularly and respond immediately if additional information is requested.

Q3. Can NCRP recover my money? NCRP itself does not directly recover money — it is a reporting and coordination platform. What it does is enable the investigation process and banking coordination that can lead to fund freezing and eventual recovery. Money recovery depends on how quickly you reported, whether funds are still in the banking system, and the success of the investigation. Early reporting gives the best chances; delayed reporting significantly reduces them.

Q4. What is the 1930 helpline? 1930 is India’s dedicated financial cybercrime helpline. It is specifically designed for urgent financial fraud reporting — when you have just lost money and want to freeze the destination account before funds are withdrawn. Call 1930 immediately after discovering fraud, before filing on the NCRP portal. The helpline operates with direct bank coordination capability. Have your transaction details ready when you call.

Q5. How long do cybercrime investigations take? This varies enormously. Simple cases with clear evidence, domestic perpetrators, and KYC-verified accounts can see FIR filing within weeks and arrests within months. Complex cases involving organized fraud, multiple mule accounts, cryptocurrency, or overseas operators can take a year or more. The victim’s cooperation, documentation quality, and the investigating officer’s workload all affect timelines. Follow up consistently and in writing.

Q6. Can I report cryptocurrency scams on NCRP? Yes. Crypto fraud is reportable on NCRP under financial fraud. For crypto cases, provide all available information: the platform URL, your transaction records, blockchain transaction hashes (TXIDs), wallet addresses of the fraudster, exchange screenshots, and all communication records. The more complete your documentation, the better the chance of blockchain tracing by investigating authorities.

Q7. Can UPI fraud be reversed? UPI transactions themselves are technically irreversible once processed. However, if the receiving account is frozen before the fraudster withdraws funds, the amount can be transferred back to the victim through a bank reversal process coordinated by the cyber cell. This is why calling 1930 within the first hour is so critical — it is the window during which reversal-equivalent recovery is most possible.

Q8. Can complaints be withdrawn from NCRP? Once filed, NCRP complaints become part of the criminal investigation system. You can contact the investigating cyber cell to inform them if you have resolved the matter privately, but formal withdrawal of a criminal complaint is a legal process that typically requires appearing before the relevant police or judicial authority. Do not withdraw complaints based on pressure from fraudsters — this is a common tactic they use.

Q9. What if I entered wrong details in my NCRP complaint? You cannot edit a submitted complaint directly. Contact the state cyber cell to which your complaint was assigned and submit a written correction with the correct details and your acknowledgment number. Do this as soon as you notice the error — incorrect details can delay or misdirect the investigation.

Q10. Is there a time limit to file an NCRP complaint? There is no fixed portal deadline, but every hour of delay reduces recovery chances dramatically. For criminal proceedings, limitation periods under law can apply to some offences. More practically, banking coordination becomes impossible once funds are withdrawn and dispersed. File as immediately as possible — ideally within the first hour, certainly within the first 24 hours.

Conclusion

NCRP and the 1930 helpline are among the most powerful tools available to Indian cybercrime victims. Used quickly and correctly, they can freeze fraudulent accounts, trace perpetrators, and initiate recovery.

If fraud just happened to you right now:

- Call 1930 immediately

- Do not delete anything

- Note every transaction detail

- File on cybercrime.gov.in

- Register an FIR at your local police station

- Save your acknowledgment number

- Follow up every 10 days

Realistic expectations: Early reporting gives real recovery chances. Delayed reporting makes recovery difficult. No outcome is guaranteed, but every complaint filed contributes to the national system that is tracking and prosecuting cybercriminals across India.

Prevention is always better than recovery. Save 1930 in your contacts today. Bookmark cybercrime.gov.in today. And share this guide with someone who might need it.

Disclaimer: This article is for educational and informational purposes only. It does not constitute legal advice. Procedures and portal features may be updated by the government. Always refer to the official cybercrime.gov.in portal for the most current information.